Business

How tax waiver, FX stability pushed pharma firms’ profits to decade-high

Nigeria’s pharmaceutical manufacturers have delivered their strongest earnings in at least a decade, signalling a sharp reversal from years of margin squeeze buoyed by currency volatility and steep import dependence.

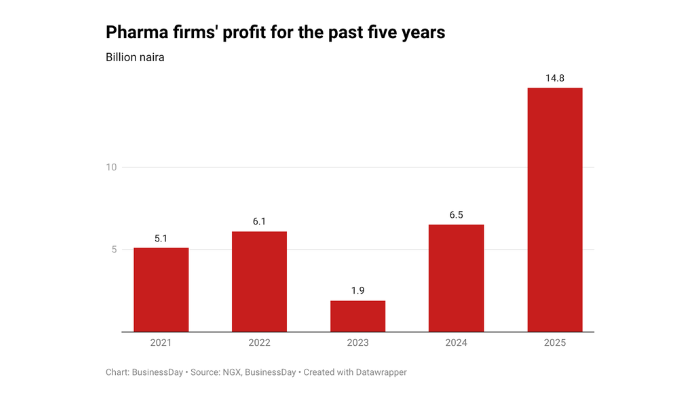

Drug manufacturers listed on the Nigerian Exchange Limited more than doubled their full-year incomes in 2025, rising from N6.5 billion in 2024 to N14.8 billion, thanks to the stability of the naira and tax waivers that helped sustain growth amid still weakened purchasing power.

Neimeth International Pharmaceuticals delivered the most dramatic swing. The company moved from a N885.3 million loss in 2024 to a N982.1 million profit in 2025, reversing consecutive years of red ink.

Valentine Okelu, managing director and chief executive officer of Neimeth International Pharmaceuticals, directly linked the turnaround to the waiver.

“The era of losses has ended. Neimeth has returned to profitability. The implementation of the Federal Government’s tax waiver for pharmaceutical raw materials has assisted in reducing production costs and accelerating organisational growth. 2025 marked a decisive turnaround,” Okelu said at a media parley earlier this month.

The financials support his position. Neimeth’s gross profit rose to N3.3 billion, while the cost of sales fell to N2.5 billion from N4.0 billion in 2024, a rare contraction in input costs in an inflationary environment.

Fidson Healthcare Plc, the sector’s largest listed player, posted a 61 percent increase in profit after tax to N9.31 billion in 2025. Gross profit expanded to N49.1 billion from N35.1 billion a year earlier, reflecting stronger margin protection despite elevated operating expenses.

May & Baker Nigeria Plc also reported record earnings, with profit after tax rising to N4.45 billion in 2025. Gross profit climbed to N13.1 billion, supported by improved domestic demand and supply gaps created by multinational exits.

Patrick Ajah, managing director of May & Baker, described the waiver as critical but cautioned against policy inconsistency.

“The executive order on customs duties and raw materials for local producers has been waived by the government. It’s fantastic, and it needs to be continued. But we need consistency. We need to increase capacity for local companies to take care of our people instead of depending on foreign companies,” Ajah said.

Tax reliefs to the rescue

At the centre of the rebound is a Presidential Executive Order signed on June 28, 2024, and implemented on March 5, 2025, which exempted 875 pharmaceutical raw materials from Value Added Tax (VAT) and import duties.

Muhammad Ali Pate, the coordinating minister of Health and Social Welfare, said that “the Order introduces zero tariffs, excise duties, and VAT on specified machinery, equipment, and raw materials, aiming to reduce production costs and enhance our local manufacturers’ competitiveness,” including specified items like Active Pharmaceutical Ingredients (APIs), excipients, other essential raw materials required for the manufacturing of crucial health products like drugs, syringes, and needles; Long-lasting Insecticidal Nets (LLINs); and Rapid Diagnostic Kits, among others.

For an industry that imports roughly 95 percent of its active pharmaceutical ingredients (APIs), the policy has altered cost dynamics almost overnight.

Drug makers grappled with a punishing cycle in which naira depreciation, port charges, and rising input costs wiped out operating gains. That cycle appears to have vanished.

FX stability drives earnings growth

Tax relief alone did not drive the 2025 earnings surge. Relative foreign exchange stability prevented a repeat of the sharp translation losses recorded in 2024.

Neimeth reported a foreign exchange gain of N48.1 million in 2025, compared with a loss exceeding N2 billion the previous year. Fidson’s net exchange difference moderated year-on-year, reflecting reduced volatility in the naira, which closed 2025 around N1,448 per dollar.

The combined effect of duty exemptions and FX stability allowed cost savings to flow directly to the bottom line. This dynamic was largely absent during the peak of the currency crisis.

Muda Yusuf, chief executive officer of Centre for the Promotion of Private Enterprise, said pharmaceutical manufacturers are among the clearest beneficiaries of the reform cycle.

“The stability in the forex market and the gradual shift toward local substitutes give an advantage over those who are importing. The government introduced waivers to ease the cost of importations for pharmaceuticals; these segments are likely to record stronger returns on investment under current reform conditions,” Yusuf said.

The key takeaway for investors is that earnings improvement is now supported by both fiscal policy and macro stabilisation rather than temporary demand spikes.

The clearest illustration of this cycle appears in MeCure Industries Plc.

Unlike peers that recorded only incremental shifts, MeCure went through a sharper earnings compression in 2024 before staging a strong rebound in 2025.

In 2024, revenue grew 45 percent to N46.03 billion, but profit after tax declined 20 percent to N2.3 billion.

Weak demand did not cause the drop. It was driven by financing costs and expansion spending.

To fund new manufacturing capacity, including its Beta Lactam plant, the company relied heavily on short-term borrowings and commercial papers during a period of aggressive monetary tightening.

Finance costs more than doubled to N4.98 billion in 2024 from N2.39 billion in 2023. Its interest coverage ratio fell to 1.64 times from 3.22 times, showing that debt servicing absorbed a larger portion of operating profit.

At the same time, selling and distribution expenses jumped 110 percent as MeCure pushed aggressively to capture supply gaps created by multinational exits. Administrative expenses rose nearly 40 percent due to higher utility costs, logistics expenses, and depreciation from newly commissioned assets.

Cost of sales also increased 45.5 percent, limiting margin expansion during the build-out phase. Revenue accelerated to N77.69 billion, and profit rebounded 183 percent to N6.5 billion. Margins recovered to about 8.4 percent, close to pre-expansion levels but on a significantly larger revenue base.

The improvement reflects operating leverage. With production capacity already installed and distribution networks established, incremental revenue now converts more efficiently into profit.

MeCure is valued at about N303 billion and ranks 39th on the Nigerian Exchange by market capitalisation. Its share price closed at N75.85 as of February 27, 2026. The stock is down 10 percent from its last close but remains up 16.3 percent year to date from N65.20.

Across the industry, firms are reinvesting improved earnings into production capacity.

Fidson allocated N7.83 billion in 2025 to expand its World Health Organisation compliant facility. Neimeth secured approval for a N20 billion capital raise to complete its Amawbia plant. May and Baker invested N6.37 billion in property, plant, and equipment to scale branded generic production.

The spending pattern shows manufacturers are attempting to lock in the benefits of the waiver before it expires in March 2027.

The strategy is clear: convert temporary tariff relief into permanent capacity expansion.

Despite the profit surge, structural vulnerabilities persist.

Nigeria’s dependence on imported medicines has declined from about 70 percent to 60 percent, according to regulatory authorities, signalling progress but underscoring continued exposure to external shocks.

The National Agency for Food and Drug Administration and Control’s 5-plus-5 policy has accelerated localisation by limiting final renewal for importers before requiring local manufacturing or partnerships.

Mojisola Adeyeye, director-general of NAFDAC, said more than 30 percent of new pharmaceutical firms emerged from that framework.

However, long-term resilience will depend on sustained investment in local active ingredient production and deeper integration of pharmaceutical value chains.

The data shows a decisive shift in earnings direction for listed pharmaceutical firms.

Tax incentives lowered input costs. FX stability reduced volatility. Capacity investments improved revenue conversion into profit, leading to enhanced operational efficiency and increased market competitiveness.

The sector has moved from margin compression to measurable profitability expansion.

For investors, the key signal is visibility. Earnings are no longer driven purely by currency swings but by operating scale and policy alignment, indicating that companies are now able to leverage their efficiencies and strategic initiatives to enhance profitability.

Healthcare is emerging as a stronger structural theme within the Nigerian equity market as manufacturers demonstrate that expansion risk taken during the downturn is now delivering returns, particularly through increased production capacity and improved healthcare services that meet rising demand. (BusinessDay)

-

News18 hours ago

News18 hours agoGunmen abduct eight charcoal burners in Plateau

-

News18 hours ago

BREAKING: El-Rufai To Remain In Custody As Court Adjourns Bail Application To April 14

-

Politics16 hours ago

Akpabio declares three Senate seats vacant, INEC to conduct by-elections

-

News16 hours ago

$6bn in 4 hours: Atiku slams Tinubu, Senate, calls it ‘reckless urgency’

-

Metro18 hours ago

Nigerian man arrested in India with N290m illicit drugs

-

Politics16 hours ago

ADC alleges plot to stage ‘Mark must go’ paid protest Thursday

-

Metro16 hours ago

Driver Of Emir Sanusi’s Wife Remanded Over Alleged Jewellery Theft

-

News16 hours ago

Sule Lamido, Sons’ Fresh Arraignment In Alleged N1.3bn Fraud Case Stalled