Business

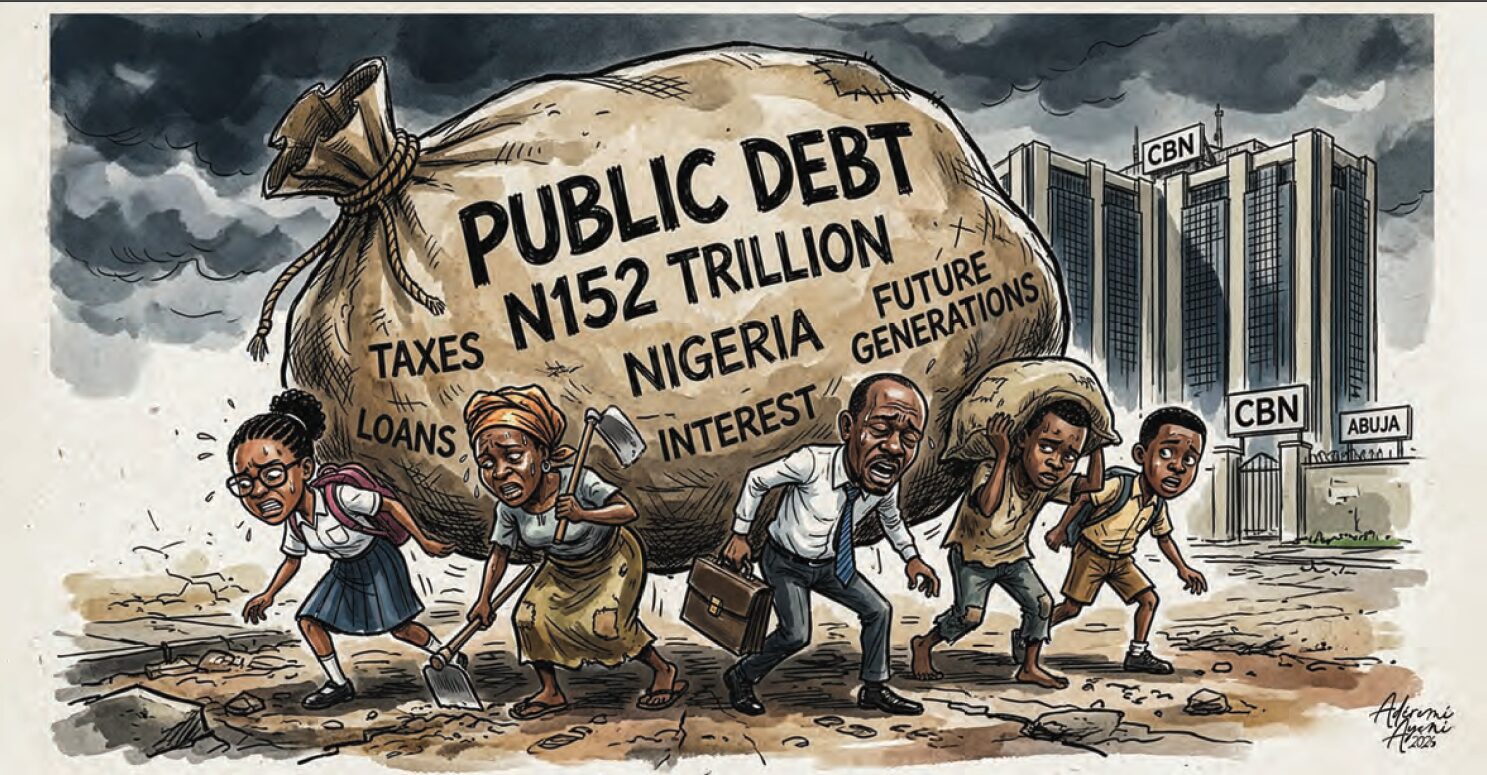

Debt without end

Nigeria has, in recent years, acquired an unenviable reputation for relentless borrowing. The frequency and scale of public debt accumulation have become defining features of fiscal policy, prompting concern among citizens who were raised on the admonition that “he who goes a-borrowing goes a-sorrowing.” That proverb was not merely moral instruction; it was an early lesson in prudence. Debt is neither free nor benign. It carries obligations that must ultimately be honoured. Those who express unease about the trajectory of public borrowing do so not out of cynicism, but from a legitimate concern for the country’s long-term stability.

A dispassionate review of the data is instructive. When President Goodluck Jonathan transferred power to President Muhammadu Buhari in 2015, Nigeria’s total public debt stood at approximately N12.06 trillion (about $63.5 billion at the time), encompassing both domestic and external liabilities. Though significant, this figure was modest relative to subsequent developments.

By May 2023, at the conclusion of President Buhari’s tenure, public debt had risen to N87.38 trillion — an increase of more than sevenfold in eight years. Borrowing had become a principal instrument for financing budget deficits and infrastructure commitments.

Under President Bola Ahmed Tinubu, inaugurated on 29 May 2023, the upward trajectory has continued. Within 23 months, the debt stock climbed to N142.3 trillion by September 2024 and surpassed N149 trillion by mid-2025. According to the National Bureau of Statistics, total public debt reached N152.39 trillion in the second quarter of 2025, divided almost evenly between domestic and external obligations. Lagos State carries the largest subnational debt burden. With fresh loan requests before the National Assembly, projections suggest the total could exceed N182 trillion in the near term.

Nigeria’s creditors constitute a complex mix. Domestically, the government borrows from the Central Bank of Nigeria — particularly through Ways and Means advances — as well as from commercial banks, pension funds, and insurance companies investing in government securities. Externally, Nigeria relies on multilateral institutions such as the World Bank, the International Monetary Fund, IMF, and the African Development Bank, AfDB, in addition to bilateral creditors including China’s Exim Bank. Eurobond holders also account for a substantial portion of external exposure.

Official justification for sustained borrowing centres on bridging fiscal deficits, financing infrastructure, stabilising the economy amid oil price volatility, managing exchange rate pressures, and refinancing maturing debt. While these objectives are legitimate in principle, critics argue that a substantial proportion of borrowing funds recurrent expenditure rather than productivity-enhancing investment. This distinction is critical to long-term sustainability.

Measured against gross domestic product, Nigeria’s debt ratio remains comparatively moderate. The mid-2025 public debt stock of approximately $97.1 billion translates into a debt-to-GDP ratio projected by the Central Bank to hover around 34.7% by the end of 2026 — a level considered technically sustainable by international benchmarks. Yet sustainability is not determined by ratios alone. It depends fundamentally on revenue strength, institutional capacity, currency stability, and the economic returns generated by borrowed funds.

Legislative approvals have facilitated the expansion. In November 2024, the National Assembly authorised N1.77 trillion ($2.2 billion) in external borrowing to support the 2024 budget. In October 2025, it approved an additional $2.35 billion, partly for refinancing Eurobonds and partly to finance the 2025 deficit. In May 2025, the Federal Government sought authorisation for a multi-currency package comprising $23.5 billion, €2.2 billion, ¥15 billion, and N757.9 billion — an aggregate of roughly N45 trillion.

Comparatively, Nigeria’s debt profile is not the most severe globally. Advanced economies such as Japan, the United Kingdom, and the United States maintain far higher debt profiles. However, those economies benefit from deeper financial markets, reserve currencies, diversified production bases, and stronger institutional buffers. Within Africa, Nigeria ranks among the three most indebted countries, alongside South Africa and Egypt, accounting for a substantial share of the continent’s external liabilities.

The central question, therefore, is not merely whether Nigeria’s debt is “safe” on paper, but whether it is sustainable in practice. Debt servicing consumes a large proportion of government revenue, constraining fiscal space for health, education, and social protection. External liabilities expose the country to exchange rate risk, particularly amid naira volatility. The rapid pace of borrowing, following the substantial expansion under the previous administration, also raises concerns about intergenerational equity.

Borrowing, when judiciously deployed, can catalyse growth and structural transformation. When it becomes habitual and disconnected from revenue reform or expenditure discipline, it can erode fiscal resilience. Nigeria’s debt trajectory is ultimately a reflection of policy choices — choices that will shape economic opportunity, institutional credibility, and the welfare of future generations.

If Nigeria continues accumulating foreign and domestic debt without undertaking the reforms required to stabilise its public finances, the phrase, “Debt Without End” may move from a dramatic warning to an unavoidable fiscal reality. Growing obligations, weak revenue, and costly debt servicing risk locking the country into a cycle where loans are used simply to stay afloat. The consequence is a shrinking fiscal space in which essential spending on infrastructure, education, health, and social services is crowded out by repayment pressure. Without corrective action, rising debt may become both unsustainable and economically constraining, limiting Nigeria’s ability to invest in the future.

Nigeria needs to shift toward a more disciplined and growth‑oriented financial strategy through the cutting of wasteful spending and ensuring that any borrowing is tied to projects capable of generating measurable economic returns. Strengthening institutions, enhancing transparency, and diversifying the economy, particularly through manufacturing, agriculture processing, and technology, will reduce dependence on volatile oil revenues. At the same time, attracting investment rather than relying on loans can create jobs and expand the tax base. With these steps, the country can manage its debt responsibly, restore fiscal stability, and gradually reduce the need for continuous borrowing. (BusinessDay)

-

News18 hours ago

News18 hours agoMilitary brass ignored Abacha’s burial plans, lobbied for succession – Abdulsalami

-

Sports18 hours ago

FIFA must never compromise football’s universality – Sepp Blatter

-

News18 hours ago

Nigerian youths condemn Major Gen Rabe Abubakar’s killing

-

Metro18 hours ago

Appeal Court’s President under fire over special Saturday sitting in hometown

-

News22 hours ago

Rtd General Rabe Laid To Rest In Katsina

-

News18 hours ago

Abiola died while Abubakar tried to secure his release —Obasanjo

-

News22 hours ago

‘Houses, grants could be yours’ — Dikko Radda woos bandits with reintegration offer

-

Politics18 hours ago

2027: APC shuts door on primary results review