Business

Nigeria’s gas riches lure Europe, but pipelines aren’t ready

European energy officials are scrambling for alternative suppliers after strikes on QatarEnergy’s Ras Laffan facility forced the company to declare force majeure on liquefied natural gas contracts with Belgium, Italy, and Poland.

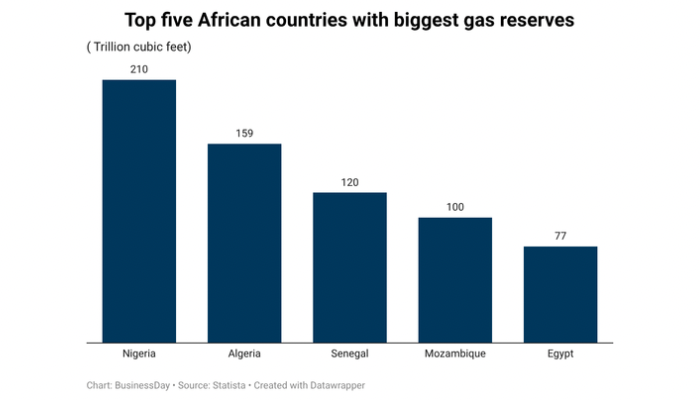

Nigeria consistently tops their shortlists. With Africa’s largest proven gas reserves and Atlantic shipping routes completely insulated from the chaos enveloping the Strait of Hormuz, the country offers a clear geographic and strategic advantage.

Yet, featuring on a spreadsheet and actually loading a tanker are two entirely different realities.

Ambassadors from multiple European capitals have held quiet conversations with Nigerian government officials in recent weeks, according to people familiar with the discussions, pressing Abuja to consider how the country’s vast gas resources, conservatively estimated at over 600 trillion cubic feet, might help plug a supply gap that is growing more urgent by the day.

The last Qatari cargoes bound for European ports arrived in the UK and Italy around March 27, according to Kpler vessel-tracking data, leaving the continent scrambling as the storage refill season approaches.

Nigeria, for its part, wants the business. What it cannot immediately offer is the infrastructure to deliver it at scale.

“Nigeria has the resources and political intent to expand gas exports, but lacks the immediate infrastructure and regulatory consistency to meet a sudden surge in European demand,” said Ayodele Oni, partner and chair of Bloomfield LP’s Energy and Natural Resources Practice Group, one of Nigeria’s leading energy law firms.

Oni added, “The federal government’s push to attract investors and the proposed Trans-Saharan Gas Pipeline, a roughly $20 billion project designed to carry about 30 billion cubic metres a year to Europe, underlines a long-term strategy to link Nigeria’s gas to European markets.

Yet current LNG plants are operating near capacity, and large projects will take years to complete.”

The scale of Europe’s predicament has sharpened quickly. Since Iranian authorities effectively restricted movement through the Strait of Hormuz beginning February 28, roughly 20 percent of global LNG flows have faced elevated geopolitical risk.

Asian buyers, currently paying between $1 and $3 per million British thermal units above European prices on the Japan-Korea Marker benchmark, have been pulling flexible Atlantic cargoes eastward, compounding the continent’s exposure.

Laura Page, insight manager for LNG and Natural Gas at Kpler, said 11 LNG cargoes have been confirmed as diverted from Europe to Asia, with two more redirected to Egypt and one to Turkey. Belgium’s Fluxys, which operates the Zeebrugge LNG terminal, has publicly named Nigeria and the United States as the most credible alternatives to cover what it describes as an eight percent shortfall in Qatari supply.

Nigeria’s geographic position makes the argument almost automatically. At roughly 10 sailing days from European ports, Nigerian LNG cargoes avoid both the Hormuz chokepoint and the longer eastward routing that inflates costs for Persian Gulf exporters competing for Atlantic market share.

Olalekan Ogunleye, executive vice president at the Nigerian National Petroleum Company, made the pitch plainly at the CERAWeek energy conference in Houston this month.

“We are right in the middle of the market,” he said. “We are 10 sailing days from Europe, close to the Atlantic Basin and close to Asia. We see commercial opportunities on top of the fact that we have the most gas reserves in Africa.”

Nigeria LNG, in which NNPC holds the largest stake, can export up to 22 million metric tons per year, with a seventh production train targeted for completion in 2027.

NNPC has begun preliminary conversations about adding two further trains and is pursuing a separate 12 million metric ton per annum project alongside gas-based industrial hubs.

Policy gaps and pipeline dreams

The gap between ambition and execution is where Nigeria’s gas story has historically come unstuck, and industry observers say the current moment is no different.

Two projects that once promised to dramatically expand Nigeria’s LNG footprint remain effectively dormant.

The Olokola LNG project, designed to produce 12.6 million metric tonnes annually, stalled after BG, Shell and Chevron all withdrew, leaving NNPC as the sole remaining partner. The Brass LNG project, planned at 10 million metric tonnes per annum, went quiet after ConocoPhillips pulled out in 2013.

Austin Avuru, chairman of AA Holdings and a veteran of Nigeria’s upstream sector, has been blunt about what is required. “Nigeria needs to match its gas slogan with effective, measurable, policy actions to drive investments in domestic gas supply,” he said in a recent note.

The country declared a decade of gas in 2021, but the investments needed to unlock that potential have not followed at anything close to the necessary pace.

Oni, at Bloomfield, acknowledges the legislative progress but argues it needs sharper execution to translate into bankable projects.

“Nigeria has introduced meaningful policy changes, most notably the Petroleum Industry Act 2021, the National Gas Expansion Programme and various power and renewable measures, that improve the investment climate and incentivise gas development,” he said.

“To become a dependable alternative supplier for Europe, however, these reforms must be fully implemented and better coordinated. Priority actions include accelerating infrastructure financing, resolving security and operational risks, ensuring consistent regulatory enforcement, and aligning gas development with broader energy-transition goals.”

For European buyers watching storage levels and spot prices simultaneously, the honest assessment from Lagos is uncomfortable.

The near-term upside for Nigeria is real but limited, with higher revenues and improved utilisation of existing export capacity. The structural transformation that would make Nigeria a genuinely decisive swing supplier is a medium-to-long-term proposition.

“A rapid response is unlikely,” Oni said. “In the short term, Nigeria can expect only modest benefits because export infrastructure is already constrained. Over the medium to long term, with sustained investment and reform, Nigeria could materially increase exports by expanding LNG capacity, building new pipelines and improving upstream production and governance.”

What that requires, he argues, is coordinated action across the full chain, federal government policy consistency, expedited licensing from the Nigerian Upstream Petroleum Regulatory Commission, accelerated field development by NNPC and international oil companies, scaled infrastructure financing, and secured operations in the Niger Delta.

European partners, he adds, will need to bring offtake commitments and financing arrangements that make the risk calculus work for investors who have been burned before.

Italy’s prime minister Giorgia Meloni was in Algeria this week seeking gas supply alternatives, a reminder that Europe’s immediate instinct is to reach for whatever pipe is already in the ground. Nigeria’s pipes, for the most part, are still on the drawing board. (BusinessDay)

-

News23 hours ago

News23 hours agoMilitary brass ignored Abacha’s burial plans, lobbied for succession – Abdulsalami

-

Sports23 hours ago

FIFA must never compromise football’s universality – Sepp Blatter

-

News23 hours ago

Nigerian youths condemn Major Gen Rabe Abubakar’s killing

-

Metro23 hours ago

Appeal Court’s President under fire over special Saturday sitting in hometown

-

News23 hours ago

Gunmen kill 20 in Kebbi community

-

Politics23 hours ago

2027: APC shuts door on primary results review

-

Sports23 hours ago

From Bauchi to Brighton: The making of Nigeria’s new wonderkid Yohanna

-

News23 hours ago

Abiola died while Abubakar tried to secure his release —Obasanjo