Facing unprecedented debts, a high rate of poverty, a forex crisis that forced foreign investors to flee, and staggering inflation, President Bola Tinubu is depending on a selected few to revive the economy. Can they pull it off?

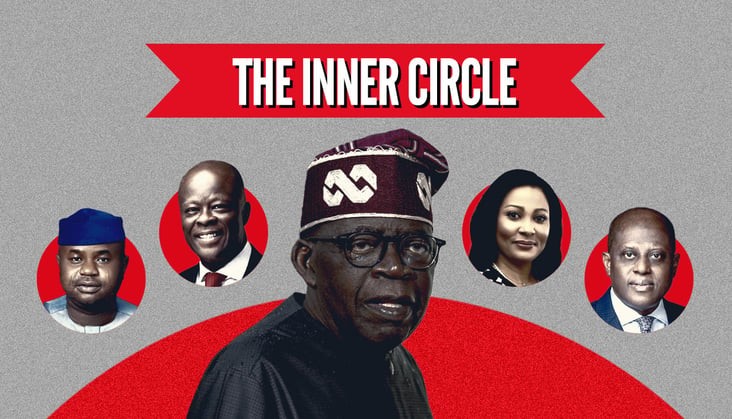

“We inherited a bad economy,” says Nigeria’s finance minister, Wale Edun, who also serves as the coordinating minister of the economy. “If we think back to the last time when the economy was stable – when it was growing, when inflation was low, and the interest rate was affordable – that period was about a decade ago.”

Edun, a veteran investment banker, must turn the tide and return the country to winning ways. President Tinubu has charged his team to “fetch water from a dry well”, he says.

This is not Edun’s first Herculean task. In 1999, after the return to democratic rule, Tinubu, then governor of Lagos State, asked Edun to turn around his state’s finances. Through a more efficient tax system and a strong partnership with the private sector, Edun succeeded.

Having campaigned on the back of this feat, Tinubu hopes to replicate the “miracle of Lagos State” on a national scale.

Edun will also have oversight of other ministries so that their actions and policies correspond with the president’s economic vision. Edun has advised the president against any further borrowing.

As many experts agree, Nigeria does not have a debt problem so much as a revenue problem: Nigeria currently collects one of the lowest amounts in the world in terms of revenue as a percentage of GDP. This is something that Tinubu’s experience in running Lagos may help with: Lagos transformed its fortunes by doubling down on the tax system in the state.

Working closely with Finance Minister Edun is Zaccheus Adedeji, who takes up his post as executive chairman of the Federal Inland Revenue Service (FIRS) in December after 90 days as acting chairman. Adedeji was already serving as the president’s adviser on revenue when he got the call to head the FIRS. Prior to his appointment, he headed Nigeria’s sugar development council and was finance commissioner in Oyo State.

Adedeji is said to have the ‘president’s ear’ – which could account for him being preferred for the job – and has advised Tinubu to “tax consumption and not production”.

Also competing for the post was Taiwo Oyedele. The high-profile tax expert has left his job as fiscal policy partner and Africa tax leader at PwC to chair the Presidential Committee on Fiscal Policy and Tax Reforms.

One of the most respected voices in the country on tax issues, Oyedele is a regular on television and has a large following for his posts on LinkedIn on fiscal matters.

Oyedele says Nigeria loses about N20tn ($25.6bn) yearly to gaps in its tax system, including evasion and certain inefficiencies in collection modes. He took a radical approach and advised the president to leverage the unique National Identification Number (NIN) of each citizen and company registration numbers to identify tax evaders. Oyedele has also said that only the FIRS should collect revenue, rather than the 62 other revenue agencies and customs.

Yemi Cardoso was appointed governor of the Central Bank of Nigeria in September. A veteran banker, he has known Tinubu for more than 30 years and worked alongside Edun on the transformation of Lagos State’s economy from 1999, where he earned the nickname ‘the headmaster’ for his love of due process.

Afterwards, he returned to the corporate sector, becoming chairman of Citibank Nigeria and co-chair of the Ehingbeti Summit, the Lagos State economic forum. Cardoso was one of the drafters of the president’s economic policy and spearheaded the current exchange-rate policy.

As the probe of the central bank continues (following Godwin Emefiele’s suspension in June), he will be tasked with implementing reforms at the apex bank and restoring public confidence in the institution. He is also expected to lower interest rates.

However, he will have to take pains to preserve the independence of the bank, which fell into disrepute under Emefiele’s stewardship.

Olatubosun (Bosun) Tijani is the minister of digital economy, a sector which accounts for at least 16% of the country’s GDP and is one of its highest employers.

Tijani accompanied the president to the G20 summit in India with a view to attracting foreign investors. His job is to ensure the creation of one million jobs in the ICT sector within two years. He has announced plans to partner with the World Bank and other organisations to train one million Nigerians.

Trade minister Doris Anite heads creating wealth and employment as well as stimulating and diversifying the economy. She supervises 16 agencies that specialise in import and export and enforcing standards. Anite was the treasurer at Zenith Bank and the finance commissioner in Imo State, which doubled its revenue.

Gboyega Oyetola is the minister of blue economy and thus in charge of the maritime sector, including seaports. The blue economy ministry was created as part of efforts to diversify the country’s economy. His job is to introduce reforms at seaports and improve the ease of doing business. The former governor of Osun State is Tinubu’s cousin and business partner.

Atiku Bagudu is the minister of budget and economic planning and is responsible for planning and designing the national budget. The former governor of Kebbi State and ex-lawmaker is a trained economist and banker. Unlike Edun, who is the darling of overseas investors, Bagudu’s integrity was compromised by having worked for the late military dictator General Sani Abacha, who stole around $5bn from the country’s treasury. Bagudu was already nominated into the president’s transition council in April.

Although not a member of the cabinet or the economic team, Mele Kyari has become a permanent feature in Tinubu’s economic forums by virtue of his position as CEO of the country’s national oil firm, the NNPC. Kyari is charged with implementing the removal of the petrol subsidy, which is a key pillar of Tinubu’s economic blueprint.

The money saved from the removal of this subsidy is expected to be invested in health care, education and infrastructure. With about 80% of Nigeria’s foreign exchange earnings coming from oil exports, the country also relies on the national oil firm to stabilise its currency.

In a bid to ensure forex liquidity, Kyari in August secured a $3bn emergency crude oil repayment loan from the African Export-Import Bank to help “stabilise the naira” and reduce petrol prices.

The NNPC boss, who was appointed by former president Muhammadu Buhari, is said to be lobbying to retain his job and was commended by the president for addressing challenges in the oil sector. Whether Tinubu retains him or not, whoever holds the position of CEO of NNPC Ltd will be an integral part of the president’s economic plan. (The Africa Report)