…FG will have to violate CBN Act to access fresh Ways & Means

…Tinubu says FG revenue hit N9.1 trillion in H1, surpasses 2023 total haul

Nigerian lawmakers have unlocked N610 billion in central bank loans to the federal government for 2024 but the same section of the law they amended to make it possible still stands in the government’s path to the cash.

The Senate last Wednesday passed a bill to amend the Central Bank of Nigeria (CBN) Act to double its Ways and Means advances to the federal government from five to 10 percent in a bid to aid the cash-strapped government’s spending plans.

Section 38 of the CBN Act had permitted only 5 percent of the previous year’s federal government revenues to be extended as loans to the government.

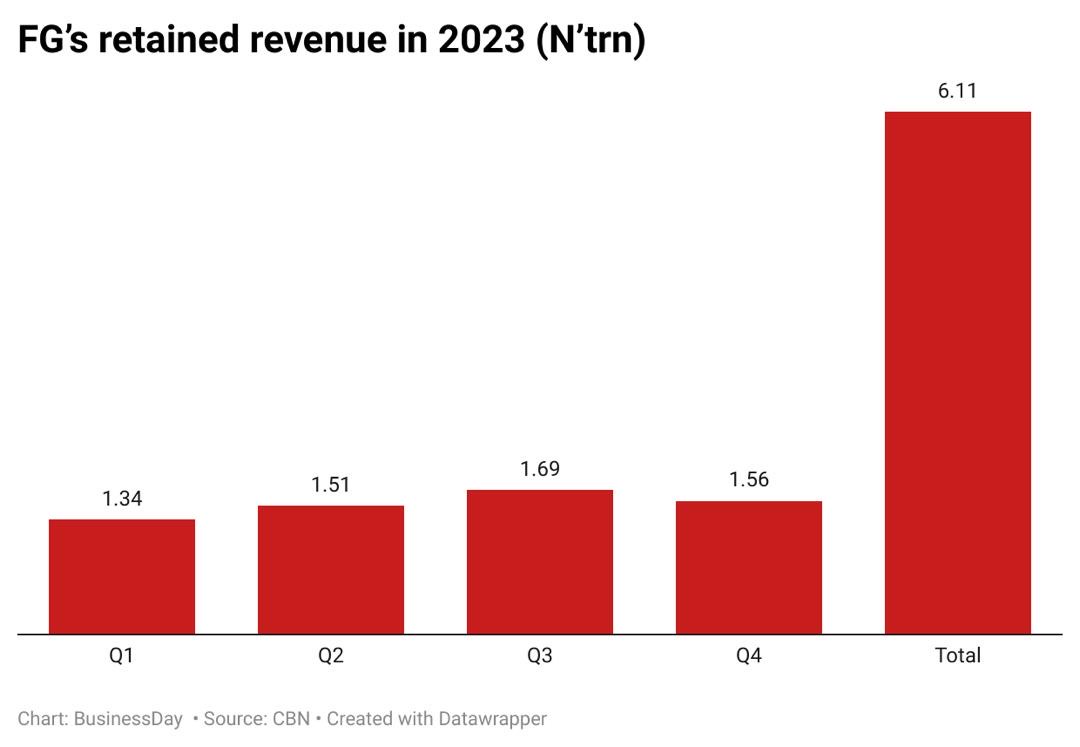

Given that the federal government earned N6.1 trillion in 2023 according to data obtained from the CBN, doubling the Ways and Means limit means the government can access 10 percent of N6.1 trillion which comes to N610 billion.

The same section of the law however states that the federal government cannot borrow from the CBN if there are any outstanding balances.

According to Section 38, sub-section 2 of the CBN Act, “All Advances made (to the federal government) shall be repaid…by the end of the financial year in which they are granted and if such advances remain unpaid at the end of the year, the power of the Bank to grant such further advances in any subsequent year shall not be exercisable, unless the outstanding advances have been repaid.”

The federal government has outstanding balances of over N30 trillion owed to the CBN, making any further borrowing from the apex bank unlawful until the outstanding has been settled.

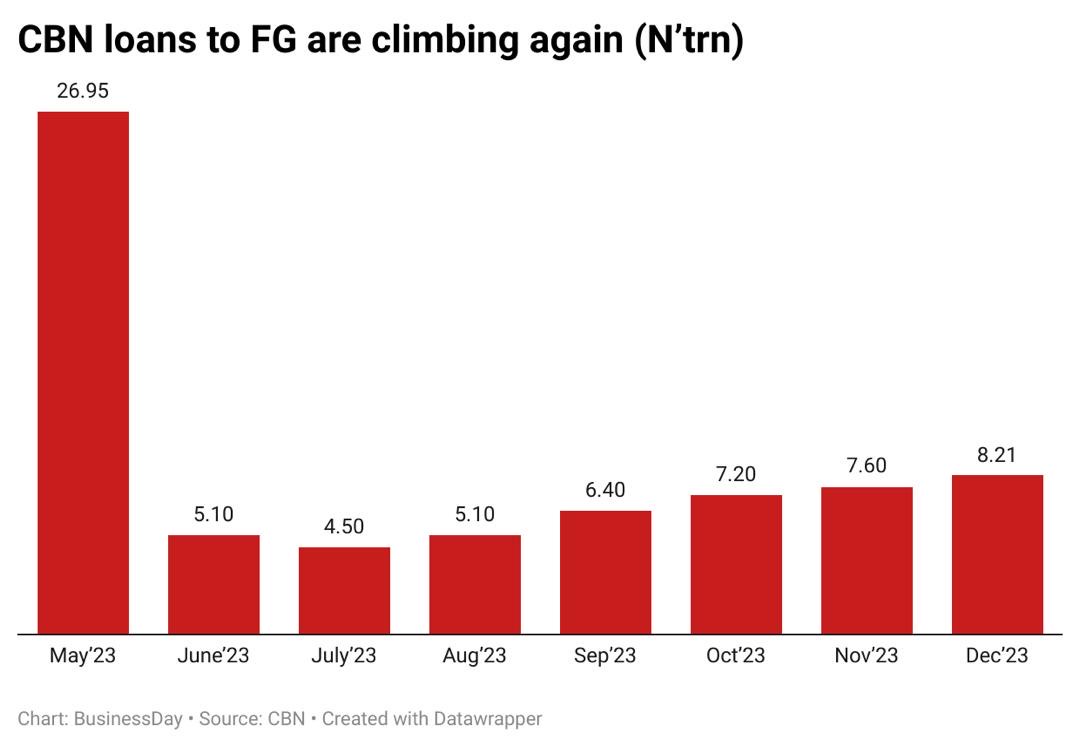

Although data from the CBN showed that the government had an outstanding balance of N8.21 trillion in Ways and Means as at the end of December 2023, but when the N22.7 trillion in securitised loans to the government is accounted for, it takes the figure to N30.91 trillion.

“The reality is that the government can no longer borrow via ways and means unless they pay back the outstanding N30 trillion,” a senior business leader told BusinessDay.

“Increasing the limit is of no consequence as it is also illegal to securitise Ways and Means to repay the CBN. What is required is comprehensive remedial legislation,” the business leader said.

Olayemi Cardoso, the CBN governor, who was appointed late last year, is well aware of what the law states and appears keen to avoid the mistake of his predecessor, Godwin Emefiele, who violated the CBN Act in giving out super-sized loans to the federal government.

He referenced the popular Section 38 of the CBN Act in making a case to lawmakers during a session where he and some members of the economic team were summoned by the Senate in February 2024, noting that the CBN would not grant any further loans to the federal government until the previous loans were repaid.

Wale Edun, minister of finance and coordinating minister of the economy, had also declared an end to the government’s recourse to CBN loans during the same session.

“I am pleased to note the fiscal authorities’ efforts in discontinuing Ways and Means advances,” Cardoso told lawmakers at the time.

“This is also in compliance with Section (38) of the CBN Act (2007). The Bank is no longer at liberty to grant further Ways and Means advances to the Federal Government until the outstanding balance as of December 31, 2023, is fully settled.”

The Cardoso-led CBN has tightened monetary policy to reign in inflationary pressure which was fuelled by a surge in money supply as a result of the outsized Ways and Means advances to the federal government.

“Empirical analysis has established that money supply is one of the factors fueling the current inflationary pressure,” Cardoso said at the time.

“For instance, an analysis of the trend of the money supply spanning over nine months shows that M3 increased from N52.01trillion in January 2023 to N68.25 trillion in November 2023 representing N16.24 trillion or 31.22 percent increase over the period,” he said.

The federal government resorted to loans from the CBN, also called Ways and Means advances, during former President Muhammadu Buhari’s administration after government revenues plummeted.

The Buhari days

Buhari’s administration inherited a N789.67 billion debt but borrowed to the hilt from the CBN in his eight-year tenure. For the first time on record, the CBN became the biggest lender to the Federal Government.

A year after he came to power, the economy slipped into recession following the collapse of global oil prices, coupled with a slump in the country’s crude oil production. Both factors slashed Nigeria’s biggest income source- oil exports.

At the end of his first term, the debt owed to the CBN stood at N6.59 trillion, up more than eightfold (735 percent) in four years.

Just over a year after the start of his second term, the economy slid into another recession amid the COVID-19 crisis and the Saudi Arabia-Russia oil war, which led to a sharp drop in oil prices.

By October 2022, the debt owed to the central bank had ballooned to N23.77 trillion, more than 30 times what the administration met in 2015.

Buhari said the funding enabled the government “to meet obligations to lenders, as well as cover budgetary shortfalls in projected revenues and/or borrowings.”

On Buhari’s watch, the federal government’s borrowing from the apex bank repeatedly exceeded the statutory limit of five percent of the previous year’s revenues.

The government failed to heed warnings from the World Bank and the International Monetary Fund (IMF), among others, about the dangers of its continued reliance on CBN financing.

In May 2023, as the curtains fell on Buhari’s time in power, some N22.7 trillion in CBN loans was securitised and converted into a 40-year bond at 9 percent per annum to reduce its strain on the federal government which had been paying the benchmark interest rate of 18 percent at the time, plus 3 percent, making a total of 21 percent per annum in interest payments.

Lawyers and financial experts argue that the securitisation of the Ways & Means is unlawful as there’s no provision allowing the government to convert loans from the CBN into securities.

Securitisation of the N22.7 trillion CBN Ways & Means is not the only infraction made by former President Buhari. The amount in itself exceeded the five percent of previous year’s revenues stipulated in the CBN Act.

Could lightening strike twice?

Some analysts fear the government may yet again breach the CBN Act to shore up badly-needed revenues.

Violating it again will undo efforts of the central bank to tame spiraling inflation by hiking interest rates by a record to its current level of 26.75 percent.

“It was the reckless resort to printing money that put Nigeria in this mess in the first place,” an economist, who did not want to be named, said, referring to the impact of the CBN Ways and Means on the country’s 28-year high inflation rate.

Breaching the CBN Act to borrow more than permissible from the bank could mean biting more than it can chew for the federal government, which will have to pay nearly 30 percent (current monetary policy rate of 26.75 percent plus 3 percent) per annum on the loans, higher than the 21 percent paid by Buhari.

The economists, who spoke to BusinessDay, were of the view that the government was focused on the wrong possible source of extra cash to fund its budget.

Tinubu says FG revenues hit N9.1 trillion in H1

The government plans to spend N27.5 trillion this year with revenues projected at N18.32 trillion.

President Bola Tinubu said during a broadcast on Sunday, August 4, that the federal government had grown its revenues to N9.1 trillion in the first half of 2024, that’s more than the total revenues earned in the whole of 2023.

It also puts the government on course to meeting its revenue projection for the first time in over a decade.

Economists however say President Bola Tinubu is still dancing around the edges with regards to growing revenues substantially.

They say the president is not going all out to increase the country’s oil revenues, which have continued to dwindle due to low production even at a time of relatively high oil prices.

“Tinubu is letting the elephant in the room off easy,” a foreign investor told BusinessDay. “Nothing shows that Nigeria is still a petrostate when its oil revenues have collapsed to the point that they have now being easily overtaken by non-oil revenues but the president (who also doubles as the minister of petroleum) doesn’t seem to be so keen to deal with the rot in the system,” the foreign investor said.

While some economists who spoke with BusinessDay said addressing the oil and gas sector is seen as a short to medium-term solution to improving revenues, one economist noted that, “Domestic revenue mobilisation through tax reforms is the most critical way of funding the budget and long-term development.”

(BusinessDay)