Business

What does it means for HoldCos to be a “Source of Strength” for banks?

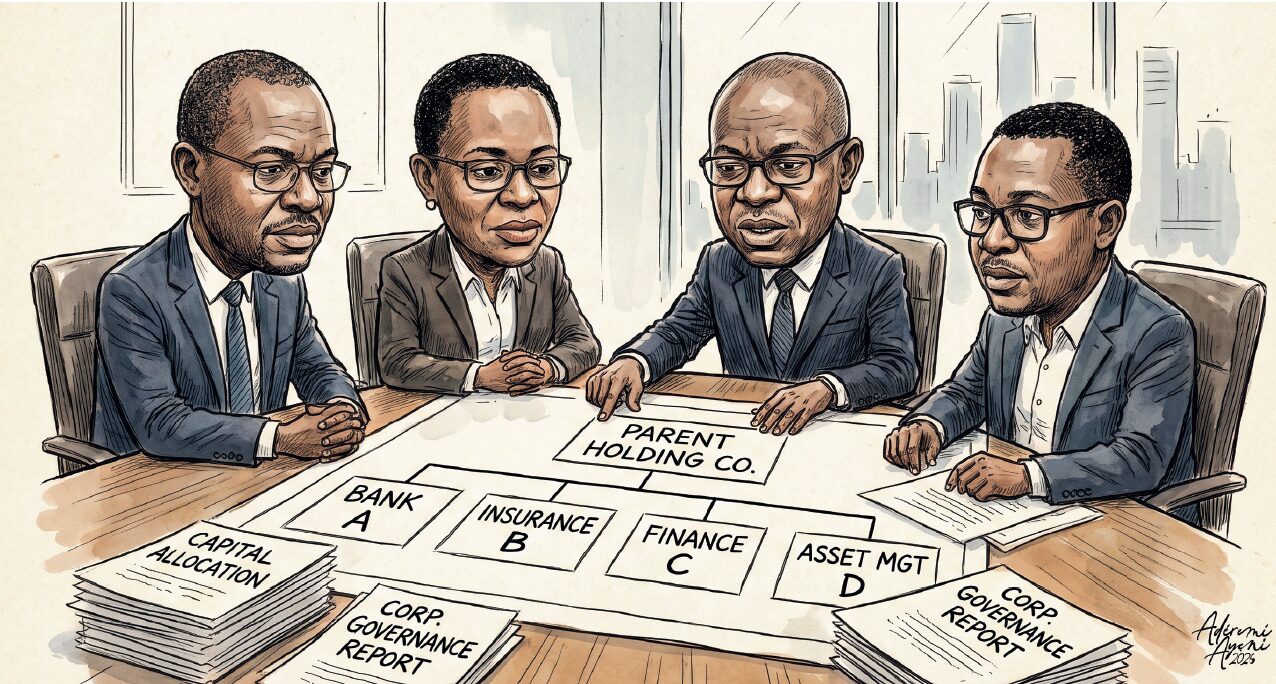

The most consequential provision in the Central Bank of Nigeria’s proposed Financial Holding Company Guidelines may not be the restructuring rules, the governance restrictions or even the tighter controls on intra-group transactions. It is the introduction of a simple but powerful idea: a financial holding company should be a source of financial strength to its subsidiaries.

The proposition appears straightforward. A parent company should support its subsidiaries. The regulatory implications, however, are far-reaching. They affect how much capital a holding company must maintain, how group resources are deployed and how regulators approach responsibility within banking groups.

The proposal is also striking because it appears to pull in two directions. On the one hand, the CBN continues its long-running effort to move financial holding companies away from the corporate parenting model of business operator towards that of financial controller. On the other hand, it expects those same holding companies to stand ready as reservoirs of capital whenever subsidiaries come under stress.

The core of the proposal is a new capital framework. The exposure draft requires a holding company’s paid-up capital and share premium to exceed the combined capital of all its subsidiaries by at least 20 per cent. It also requires the holding company to satisfy the capital adequacy ratio applicable to its most significant subsidiary, both on a standalone and consolidated basis. These requirements are cumulative. The result is a substantially more conservative capital structure than under the current framework.

To understand the significance, consider the current prudential regulations governing Nigeria’s banking system. The CBN already requires Nigerian banks to maintain capital adequacy ratios of between 10 per cent and 15 per cent, depending on their licence category. These ratios are already above the Basel III minimum total capital requirement of 8 per cent before additional conservation and countercyclical buffers are applied. The proposed 20 per cent holding-company capital buffer is therefore layered on top of an already more conservative prudential framework.

Furthermore, the capital buffer applies to 100 per cent of subsidiary capital requirements irrespective of economic stake. Thus, a 51 per cent stake still attracts provision of the full 20 per cent buffer, diverging from Basel’s more nuanced consolidated supervision approach, which recognises minority interests in assessing loss-absorbing capacity. The justification appears to lie in the responsibilities attached to control. The strategic benefits of being the controlling shareholder are expected to carry a correspondingly higher level of prudential responsibility.

The new capital buffer is proposed to effect the “source of strength” principle. The doctrine originated in the United States during the 1930s and evolved through supervisory practice rather than through a single legislative design. American regulators take the view that holding companies should serve as a source of financial support to their banking subsidiaries, a position finally codified through the Dodd–Frank reforms following the 2008 Global Financial Crisis.

Importantly, however, the doctrine has never been fully resolved in practice. Regulators have broadly agreed that holding companies should possess the capacity to provide support. They have been less successful in defining precisely when that support must be deployed and under what circumstances. This distinction matters. Requiring a holding company to demonstrate the ability to support a subsidiary is fundamentally different from imposing a legal obligation to do so. The first is essentially a provisioning requirement, while the second takes the form of a guarantee. Global regulatory practice has generally favoured the former – requiring buffers, loss-absorbing capacity and long-term funding instruments, while not mandating automatic rescue of distressed subsidiaries.

Against this background, the CBN’s proposed introduction of a hard 20 per cent capital buffer, in addition to holding-company-level capital adequacy ratio requirements, appears more ambitious than many comparable international approaches. It naturally raises important policy questions: what level of distress would justify deployment of the buffer? Would support extend equally to banking and non-banking subsidiaries? If a bank ultimately enters resolution, would institutions such as the Nigeria Deposit Insurance Corporation or the Asset Management Corporation of Nigeria have any recourse to the holding company’s capital reserve? These are issues on which greater regulatory clarity would strengthen the proposal.

None of these questions diminish the proposal’s underlying logic. The CBN has spent years tightening prudential supervision amid concerns about credit losses, governance weaknesses and systemic resilience. From that perspective, requiring controlling shareholders to place more of their own capital at risk is a rational response to moral hazard. If a holding company benefits from controlling a banking group, it should also bear a greater share of the financial responsibility when risks materialise.

Furthermore, these highly technical proposals have implications well beyond the banking system. A stronger holding-company framework can improve confidence in the financial system, reduce systemic risk and lessen the likelihood that banking distress ultimately becomes a burden on depositors or taxpayers.

The unresolved challenge is how the source-of-strength principle evolves beyond mere demonstration of financial capacity into a more substantive obligation. The exposure draft proceeds boldly on the first issue while leaving the second largely unresolved. The true meaning of “source of strength” lies in the circumstances under which reserved capital may be called upon. Another challenge is ensuring that stronger prudential safeguards do not unnecessarily constrain capital allocation or investment across financial groups. CBN’s proposal has galvanised an important conversation that will shape the future of banking regulation in Nigeria. (BusinessDay)

-

News16 hours ago

News16 hours agoTinubu silent on audit reforms five months after NASS’ passage

-

Metro16 hours ago

Metro16 hours ago‘I killed my patients to save them from suffering,’ says doctor who murdered 15 people

-

Politics15 hours ago

Adeleke’s Achievements Will Secure His Re-Election – Igbalaye

-

News16 hours ago

Sirika did not sign contract documents – EFCC witness tells court

-

Politics16 hours ago

Legal distractions, ‘intimidation’ weaken opposition’s 2027 contest

-

News15 hours ago

Tinubu outspends Buhari on corruption fight, but is he winning the war?

-

Politics16 hours ago

ADC bars state chapters from handling court cases

-

Business16 hours ago

Nigerian investors gain N3.45 trillion as equities market surges