Over the last five financial years, Oando has recorded a positive net operating cash flow only once, in 2023. This is a cause of concern as it raises questions about the company’s ability to generate sustainable cash from its core operations and reliance on external financing to stay afloat.

Last year, Oando reported a negative net operating cash flow (NOCF) of N545.5 billion, despite posting a net income of N52.5 billion. While the company achieved a positive NOCF of N148.2 billion in 2023, its cash flow performance in previous years has been less favourable.

In 2022, Oando recorded a negative NOCF of N16.5 billion, followed by negative NOCF figures of N38.8 billion in 2021 and N36.2 billion in 2020. These trends indicate a persistent reliance on external financing to sustain operations, raising concerns about the company’s cash flow sustainability.

Net Operating Cash Flow Ratio

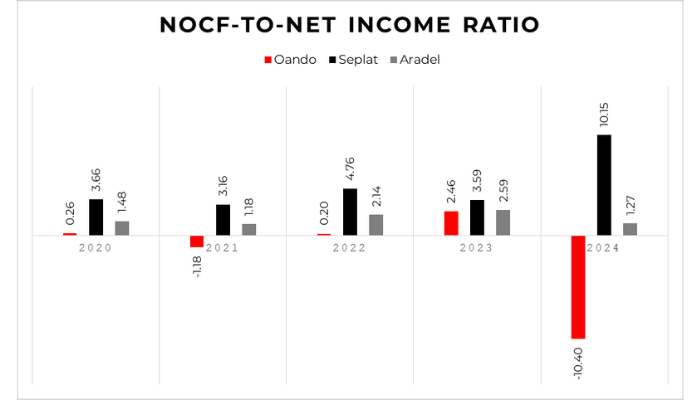

Oando’s NOCF ratio over these years gives room to these concerns, as the group posted a strong NOCF ratio only in 2023. The NOCF ratio is the operating cash flow to net income ratio. It measures a company’s ability to convert its accounting profits into actual cash flow from operations.

When the ratio is greater than 1, it shows that the group is quite efficient in generating cash from its operations. However, when the ratio is less than 1, it is suggestive that profits may be influenced by non-cash items. However, when the ratio is negative, it signals that the group may be reliant on external financing to stay afloat.

In 2020, Oando recorded an NOCF ratio of 0.26, as it posted a net loss of N140.7 billion alongside a negative NOCF of N36.2 billion. The group posted a negative NOCF ratio of 1.18 in 2021 as it posted a net profit of N32.9 billion. In 2022, the NOCF ratio was 0.20 as the group made a net loss of N81.2 billion. In 2023, the situation was much improved as the group posted a net income of N60.3 billion and an NOCF ratio of 2.46.

Last year, there was a surge in Oando’s trade receivables and current prepayments by N1.19 trillion. During the same year, the group recorded only N146.7 billion in cash from its operations. Essentially, these drove the group’s net operating cash flow to a negative N545.5 billion.

These figures shine the spotlight on Oando’s cash flow sustainability and the quality of its earnings. When juxtaposed against other upstream oil firms, it tells a concerning story for Oando’s investors.

For Seplat Energy, the company’s net operating cash flow has consistently appreciated, moving from N112.5 billion in 2020 to N535.6 billion in 2024. In terms of NOCF ratio, Seplat recorded 3.66 in 2020, 3.16 in 2021, 4.76 in 2022, 3.59 in 2023, and a whopping 10.15 as of the third quarter (Q3) of 2024, figures so good, they raise questions about Seplat’s reported revenues.

When asked if Seplat has a conservative revenue recognition policy, an anonymous staff said: “There is nothing like a conservative or aggressive revenue recognition policy at Seplat. Revenue is recognized once risks associated with the oil and gas lifting are determined to have passed onto the buyer.”

Aradel does not have a high NOCF ratio like Seplat, however, the company has strong cash flow management. Its NOCF ratio has been within acceptable limits, from 1.48 in 2020, 1.18 in 2021, 2.14 in 2022, 2.59 in 2023, and 1.27 in 2024.

In the oil and gas space, it is customary for companies to have their net operating cash flow ratio above 1. It is because of the effect of non-cash expense items such as depreciation and amortization charges on their net income.

Oando’s reliance on debts calls for concerns

Oando’s financial trajectory underscores the need for careful debt management to mitigate solvency risks. Since its entry into the upstream sector in 2014, the company has relied heavily on borrowings to finance its expansion. Its $1.5 billion acquisition of ConocoPhillips began with an upfront deposit of $435 million, largely funded by a $345 million credit facility.

The group’s reliance on debt has remained a key feature of its financial strategy, with total borrowings—both short- and long-term—rising to N2.76 trillion as of the 2024 financial year. A significant portion of this debt includes the $650 million Afreximbank loan used to finance its acquisition of NAOC (Agip), further amplifying concerns about the company’s growing debt burden.

Despite these concerns, investor sentiment toward Oando was initially optimistic. The Agip acquisition fueled excitement among shareholders, driving the stock up by 529% in 2024. However, this enthusiasm has since waned following the release of its 2024 financials, as concerns over cash flow sustainability and debt levels led to a year-to-date negative return of 4.55% on the stock.

Amid these financial pressures, Oando’s recent capital investments could offer a potential turnaround for its cash flow position. Following the Agip acquisition, Group CEO Wale Tinubu has been vocal about the company’s future prospects, emphasizing the over 1 billion barrels of oil in its reserves as a key asset. Executive Director Alexander Irune echoed this optimism, stating in a separate interview that Oando is targeting 100,000 barrels per day (bpd) production by 2028.

If the company can efficiently leverage its reserves and optimize production, it stands a chance to improve cash flow and gradually reduce its liabilities—a critical step toward long-term financial stability. (BusinessDay)