Nigeria’s conflicting fiscal deficit figures for 2024 have raised fresh concerns about the government’s transparency, a situation that could potentially unsettle investors who are beginning to find confidence in Africa’s most populous nation’s economy.

Three credible public data sources gave different figures, with the ministry of finance numbers being the lowest.

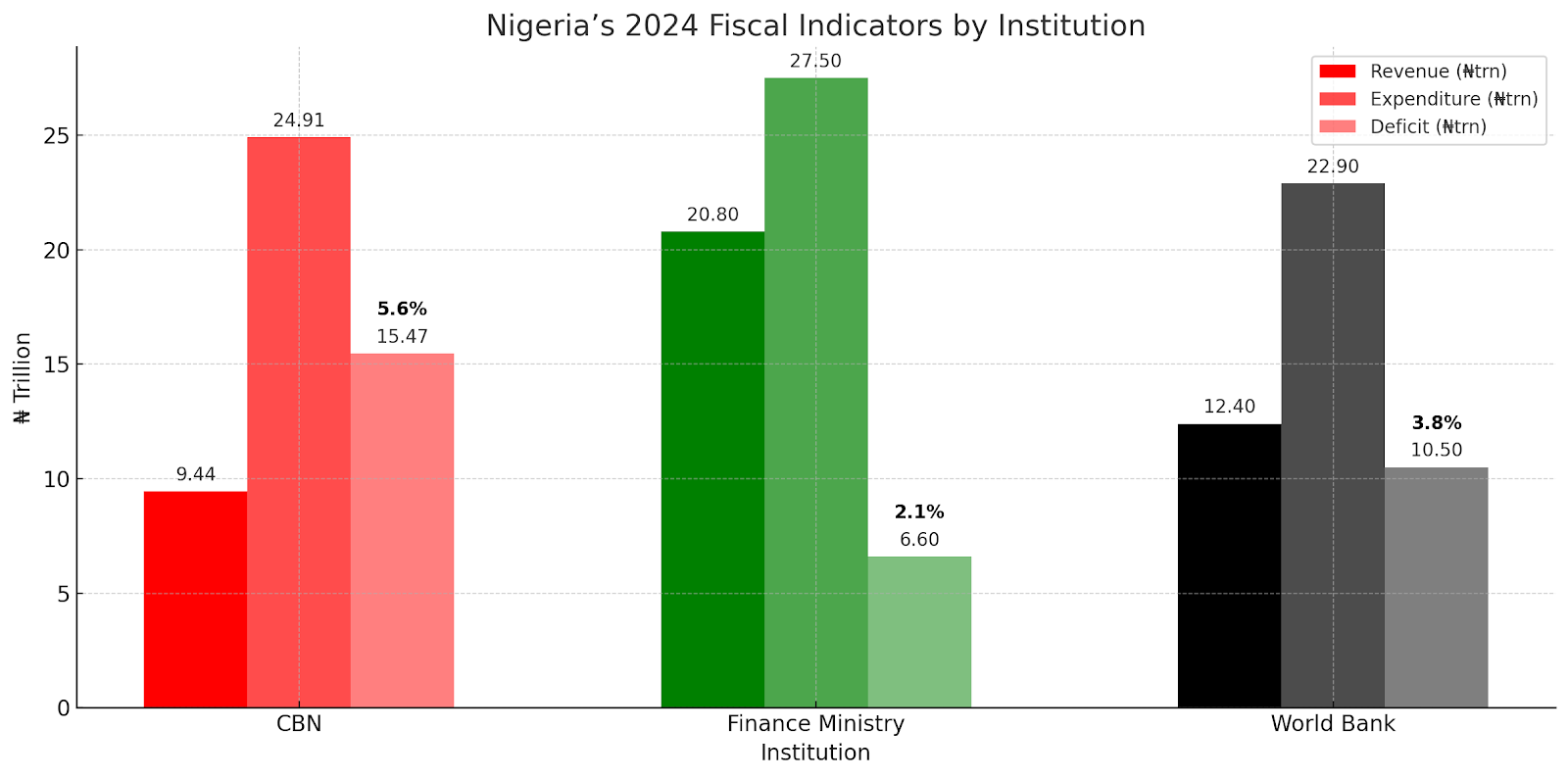

According to an excerpt presented by Finance Minister Wale Edun to investors at the April Springs Meeting, Nigeria’s fiscal deficit – the difference between the government’s total revenues and its expenditure – stood at N6.6 trillion or 2.1 percent of GDP where revenue was N20.8 trillion and expenditure at N27.5 trillion.

This however, contrasts with the position of the Central Bank of Nigeria, which revealed in its quarterly bulletin that FGN revenue stood at N9.44 trillion while expenditure was N20.8 trillion, amounting to N15.47 trillion deficit or 5.6 percent of GDP — this is more than double the data communicated by the finance ministry.

The World Bank on the other hand reports in its Nigeria Development Update, a biennial report on the country, that revenue was N12.4 trillion, expenditure at N22.9 trillion, leaving a deficit of N10.5 trillion— 3.8 percent of GDP.

Another point of variance is the difference between the finance ministry and World Bank’s 2023 data. The finance minister reports a 2023 shortfall of 4.6 percent of GDP, yet the Washington-based institution puts it at 5.1 percent.

President Bola Tinubu in his mid-term speech stated that the nation’s fiscal deficit has “narrowed sharply from 5.4% of GDP in 2023 to 3.0% in 2024” — above the finance ministry’s data both in 2023 and 2024.

BusinessDay reached out to the ministry of finance on the 26th of May, 2025 for clarity on the conflicting data but no response was received as at the time of filing this report.

“The data is relatively clear, and perhaps there are some limitations to each policymaker’s information at the time of publishing. We do, however, note that the Central Bank of Nigeria, in its role as the government’s banker, has a unique and encompassing vantage point,” said Samuel Sule, chief executive officer of investment firm Renaissance Capital Africa.

Sule stated that Nigeria, being a frontier market, continues to push a reform agenda, emphasising that investors understand this dynamic and understand that progress is non-linear with some information asymmetry.

“More progress is certainly required,” he said, stressing that Nigeria can lower its deficits by improving its revenue base and cutting its debt, which will amount to a reduction in debt service.

Wale Smith, an analyst, said that with differing fiscal data, it may be “hard to inspire confidence in Nigeria’s reform story”, urging for more coordination in published information to uphold transparency.

“For a government actively travelling the globe to court foreign capital, basic credibility starts with accurate and transparent reporting at home,” Smith said in a note on May 22 2025.

“These glaring inconsistencies across official fiscal data sources not only muddy the waters for analysts and investors but also make life unnecessarily difficult for ratings agencies.”

For financial blogger, Feyi Fawehinmi, when government key agencies’ published fiscal figures that cannot be reconciled, “they torch what little confidence remains in their stewardship of the economy”.

“The gaps here are far too wide to dismiss as quirks of capital-expenditure accounting or other technical accounting treatments. If those differences are genuine, the Finance Ministry, CBN and every other agency involved must produce a single, reconciled statement, before pushing any more numbers into the public domain,” Fawehinmi said in his post on May 14, 2025.

Meanwhile, the International Monetary Fund (IMF) projected that Nigeria’s fiscal deficit will worsen, with the government expected to spend 4.5 percent more than it earns in both 2025 and 2026.

This marks a deeper shortfall compared to 2024, when Nigeria’s General Government Overall Balance stood at -3.4 percent of GDP, according to IMF data. The deficit is projected to rise to -4.5 percent of GDP in the following two years.

“Spending, borrowing and interest rates are increasing at a more material pace than revenue” Sule said on Nigeria’s widening fiscal deficit. (Thisday)