…Sees Nigeria spending 4.5% more than revenue in 2025

The International Monetary Fund (IMF) has underscored the critical need for countries, including Nigeria, to strengthen their fiscal positions, highlighting recent energy subsidy reforms in Nigeria as a difficult but necessary step.

It admonished Nigeria to strengthen the reform with fiscal discipline.

On Wednesday, top IMF officials, speaking in Washington DC on Wednesday on the challenging global outlook, emphasised that robust fiscal policy is essential for building confidence and resilience.

Davide Furceri, a division chief in the Fiscal Affairs Department, emphasised the urgency for countries to boost domestic revenue, citing three key trends. “Foreign aid is declining,” he said. “Interest rates on debt are rising, and capital flows are drying up.”

These factors necessitate a greater reliance on internal resources. Therefore, countries must increase tax base, improve efficiency and remove exemptions, he said.

Turning specifically to Nigeria, Furceri acknowledged the significant steps already taken.

“Nigeria has managed a difficult reform,” he stated, referring to the removal of the petrol subsidy.

However, the reform journey is not complete. He outlined the ongoing priorities for the nation, noting that Nigeria “must generate more revenue through tax base expansion, spend wisely, strengthen efficiency of spending on social… and infrastructure.”

Furthermore, reducing ‘fiscal uncertainty’ through predictable and transparent policies is vital for creating a stable economic environment conducive to investment and sustainable growth.

Zeroing in on the challenges faced by emerging markets and developing economies, Era Dabla-Norris, deputy director in the Fiscal Affairs Department, noted that growth prospects have been marked down.

She identified primary risks, including policy uncertainty, escalation of geoeconomic uncertainty and lower revenues as consumption and spending slow.

To navigate these pressures, Dabla-Norris advised a path of ‘gradual adjustment’ and the need to mobilise to expand tax base, while pushing for policies that will boost growth.

A significant area for potential fiscal savings, particularly relevant for Nigeria, is energy subsidy reform.

Dabla-Norris highlighted that “energy subsidy reforms can free fiscal savings for budget support, social spending.”

However, she was clear on the IMF’s stance regarding their effectiveness as a social tool: “Energy subsidies are poor instrument to fund social spending.”

Recognising the immediate impact of price increases, she advised that countries “implement reforms in stages, eg compensate those who need it most especially in countries where trust is weak.”

This phased approach, coupled with targeted support, is seen as crucial for managing the social and political implications of such reforms.

Vitor Gaspar, director of the Fiscal Affairs Department at the IMF, painted a stark picture of the current global economic landscape.

“Global economic prospects have heightened uncertainty,” Gaspar stated, noting that “financial conditions have tightened, and global debt remains stubbornly high and rising, a trend growing higher and faster even before the pandemic.”

He pointed out that global figures often mask significant disparities, with “119 countries’ debt above pre-pandemic” levels.

He observed that “public debt in large economies is growing fast” and that “trade policy are off the charts,” contributing to an environment where “outsize risks dominate.”

“Ministers of Finance must act decisively. Fiscal policy must be anchor for confidence.” The fundamental principles, he reiterated, involve ministers needing to “tax fairly, spend wisely.”

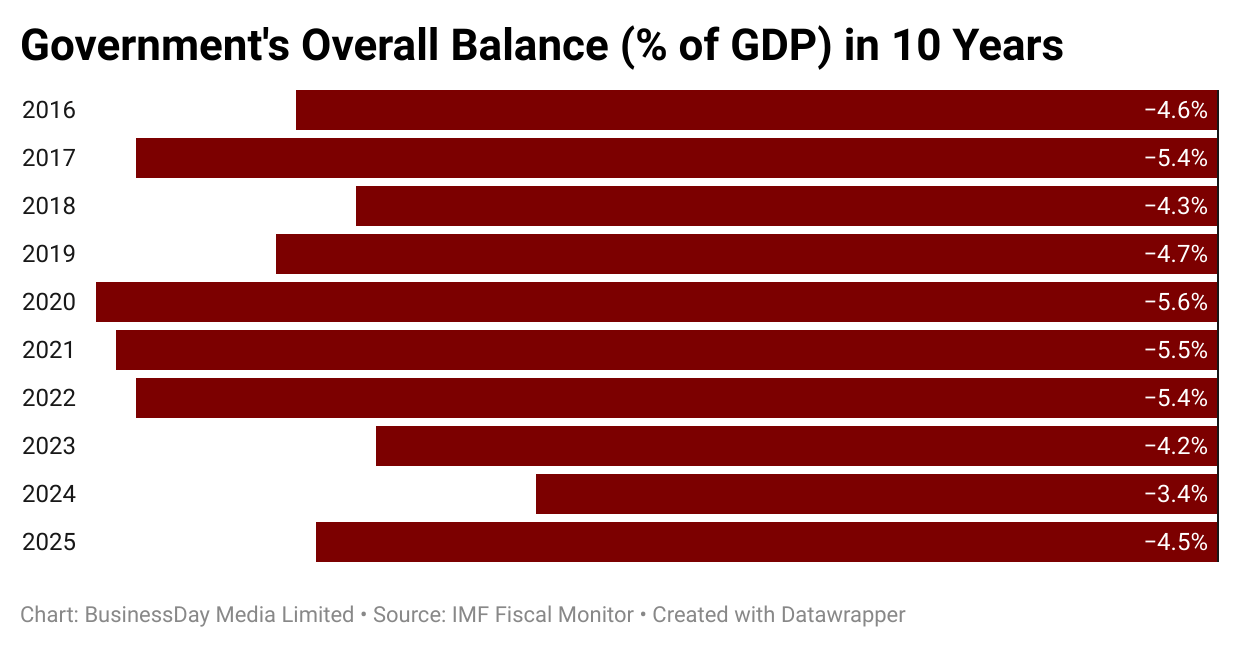

Nigeria to spend 4.5% more than it earns in 2025

The IMF also projected that Nigeria’s fiscal deficit will worsen, with the government expected to spend 4.5 percent more than it earns in both 2025 and 2026.

This marks a deeper shortfall compared to 2024 when Nigeria’s general government overall balance stood at -3.4 percent of GDP, according to the IMF data.

General government overall balance, expressed as a percent of GDP, is the difference between the government’s total revenues (from taxes, oil sales, and other sources) and its total expenditures (on salaries, infrastructure, subsidies, interest payments, etc.).

According to the IMF data, Nigeria’s general government revenue (percent of GDP) is projected to decline to 14 in 2025 and 13.9 in 2026, from 14.4 in 2024.

As of mid-2024, Nigeria’s debt-to-GDP ratio stood at 55 percent, a significant increase from 42.4 percent at the end of 2023. This uptick is attributed to factors such as exchange rate depreciation and increased domestic borrowing at higher interest rates.

The Washington D.C based Fund said global public debt will rise sharply in 2025, exceeding 95 percent of global GDP, driven by growing policy uncertainty, trade tensions, and increasing fiscal demands.

This marks a 2.8 percentage point jump, twice the 2024 estimate, and is likely to push debt levels near 100 percent of GDP by the end of the decade, surpassing pandemic-era highs.

The IMF’s latest warning came during a press briefing on the Fiscal Monitor at the ongoing IMF/World Bank Spring Meetings in Washington D.C., where officials emphasised that without a decisive policy action, global debt could rise even further. These projections are based on data from the World Economic Outlook and incorporate recent tariff announcements made between February and April 2025, which have heightened economic volatility.

“Amid significant policy uncertainty and an increasingly fragile global economy, the rise in debt is not only persistent, it is accelerating,” the IMF stated. The Fund noted that rising tariffs, tighter financial conditions and geopolitical tensions are compounding risks and putting added strain on public finances.

The IMF advised countries to implement gradual and credible fiscal adjustment plans, especially those with limited fiscal space. “Countries should put their fiscal house in order by adopting prudent policies within robust frameworks. This is critical to building public confidence and reducing economic uncertainty,” the IMF said.

For low-income and developing countries, which are already facing financing difficulties, the IMF recommended staying the course on planned fiscal reforms. This includes rationalising spending, broadening the tax base, enhancing revenue collection and ensuring that any new expenditure is met with offsetting measures. Countries in debt distress were urged to pursue timely and coordinated debt restructuring efforts.

In a worst-case scenario, the IMF warned, global public debt could surge to 117 percent of GDP by 2027, its highest level since World War II, if growth falters and revenues decline. That would exceed current baseline projections by nearly 20 percentage points. (BusinessDay)