The World Bank has approved over N13.21 trillion ($8billion) as loans for different developmental projects for President Bola Ahmed Tinubu-led federal government in the last 20 months, Daily Trust can report.

Analyses of the various loans indicated that they were targeted at several interventions in various sectors of the economy with three fresh loans amounting to $1.1 billion approved between Friday and yesterday.

Daily Trust gathered that the country’s debt profile has hit N142 trillion, according to data published by the Debt Management Office (DMO).

The 2025 budget of N54.99tn has a debt service component of N14.32tn and N13.64tn for recurrent expenditure.

Foreign exchange on the increase

This development comes as the Central Bank of Nigeria (CBN) on Tuesday reported the highest Net Foreign Exchange Reserve position as of the end of 2024.

According to the CBN data released on Tuesday, NFER stood at $23.11 billion, the highest level in over three years, Daily Trust gathered. The development marked an increase from $3.99 billion at year-end 2023, $8.19 billion in 2022, and $14.59 billion in 2021.

$2.2bn expected in 2025

Daily Trust reports that the federal government is expected to receive fresh loans from the World Bank, totalling $2.2 billion in 2025.

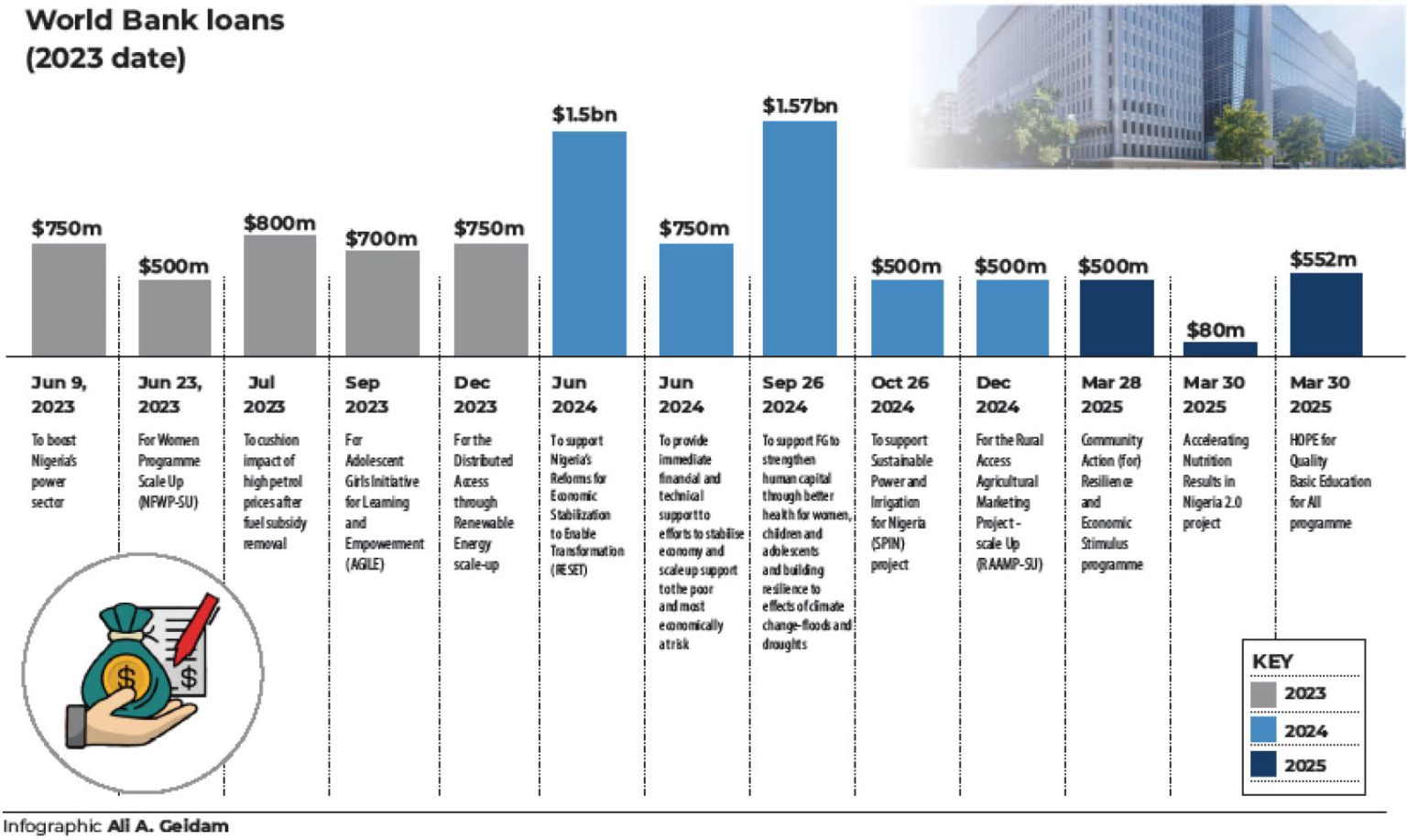

Just last Friday, the bank approved a $500 million loan to support the country’s Community Action for Resilience and Economic Stimulus Programme.

The loan was granted on March 28, 2025, under the project titled, “Community Action (for) Resilience and Economic Stimulus Program,” which aims to provide essential support to households affected by economic downturns and to bolster community resilience.

Just yesterday, the bank approved two other loans including $80m for the Accelerating Nutrition Results in Nigeria 2.0 project and $552m for the HOPE for Quality Basic Education for All programme.

Minus the $800 million support of July 2023, the federal government has in the last 20 months secured a total of $8.6 billion from the World Bank. This translates to N13.2 trillion at the current exchange rate.

LCCI expresses concerns

The Lagos Chamber of Commerce and Industry (LCCI) has expressed concern over the rising debt with the fresh loan from the World Bank.

While it acknowledged the loan’s direct impact on small businesses and vulnerable populations, through grants and livelihood support, it described the intervention as “a potential short-term stimulus.”

Director General of LCCI, Dr. Chinyere Almona, noted that Nigeria’s rising debt burden “is a growing concern, particularly given the slow pace of disbursement and implementation of previously approved loans.”

The chamber stated that with the World Bank’s share of Nigeria’s external debt reaching $17.32 billion, “the question of debt sustainability becomes increasingly pressing.”

Almona added that if the situation is not efficiently managed, “additional borrowing could exacerbate fiscal vulnerabilities, weaken investor confidence, and limit the government’s ability to execute long-term economic reforms.”

She stated that from a business perspective, while targeted stimulus programmes can offer temporary relief, structural economic challenges such as inadequate infrastructure, multiple taxation, and forex volatility remain unaddressed.

“Businesses require a stable operating environment, and while social welfare programmes are essential, they must be complemented by policies that foster productivity, investment, and job creation.

“There is also concern about the efficiency of funds allocation and utilisation, given that only 16% of previously approved World Bank loans under the current administration have been disbursed. This raises questions about the absorptive capacity of relevant institutions and the risk of funds being underutilised or mismanaged”, she said.

To maximize the benefits of this loan while mitigating associated risks, the LCCI said among other recommendations, there must be a transparent and efficient disbursement mechanism that ensures funds reach the intended beneficiaries, particularly small businesses and vulnerable communities.

It added that the government should adopt a prudent debt management strategy that prioritises concessional financing and ensures that borrowed funds are tied to projects with clear economic returns.

“The LCCI stands on the point that a more impactful stimulus for economic growth is that the government solves the perennial problem of poor power supply and high cost of energy and creates an enabling business environment where small businesses can thrive, creating jobs and generating revenues for the government.

“While the World Bank loan offers immediate relief, long-term economic resilience can only be achieved through a comprehensive strategy that fosters economic diversification, enhances productivity, and strengthens institutional frameworks for effective governance,” the statement added.

Catalogue of World Bank loans

On June 9, 2023, the World Bank approved a loan of $750 million to boost Nigeria’s power sector.

The loan with project ID: P174622 was tagged as additional financing for the Power Sector Recovery Performance-Based Operation, which was first approved on June 23, 2020.

In the same month, specifically on June 23, the World Bank approved $500 million for the Nigeria for Women Program Scale Up (NFWP-SU).

The scale-up financing was to further support the government of Nigeria to invest in improving the livelihoods of women in Nigeria.

In July 2023, Nigeria secured $800 million from the World Bank to cushion the impact of high fuel prices after the removal of fuel subsidy. The government later clarified that the $800 million was not a loan but a support from the World Bank.

In September 2023, the World Bank approved an additional $700 million for the Adolescent Girls Initiative for Learning and Empowerment (AGILE) project to improve learning outcomes of the girl–child.

The approval on-boarded 11 additional financing states which, joined the initial seven pilot states.

The states are: Adamawa, Bauchi, Gombe, Jigawa, Kogi, Kwara, Nasarawa, Niger, Sokoto, Yobe, Zamfara.

And in December 2023, the World Bank approved the Nigeria Distributed Access through Renewable Energy Scale-up (DARES) project, being financed by $750 million International Development Association (IDA) credit.

It was expected to leverage over $1 billion of private capital and significant parallel financing from development partners, Daily Trust gathered.

The financing from development partners include $100 million from the Global Energy Alliance for People and Planet and $200 million from the Japan International Cooperation Agency (JICA).

In June 2024, the World Bank released a $1.5 billion loan to Nigeria to support Nigeria’s Reforms for Economic Stabilisation to Enable Transformation (RESET) Development Policy Financing Program (DPF).

Then, another $750 million was approved for the Nigeria Accelerating Resource Mobilization Reforms (ARMOR) Program-for-Results (PforR).

The combined $2.25 billion package, according to the World Bank “provides immediate financial and technical support to Nigeria’s urgent efforts to stabilise the economy and scale up support to the poor and most economically at risk.”

On September 26, 2024, the multilateral organisation also approved three operations for a total of $1.57 billion to support the Government of Nigeria in strengthening human capital through better health for women, children and adolescents and building resilience to the effects of climate change such as floods and droughts through improving dam safety and irrigation.

Furthermore, in October, the World Bank approved a $500 million loan to support the Sustainable Power and Irrigation for Nigeria (SPIN) project aimed at reducing climate-induced challenges.

The year ended with another approval of $500 million in concessional financing for the Rural Access Agricultural Marketing Project- Scale Up (RAAMP-SU) in Nigeria, according to the Washington DC-based institution.

Multilateral loans vulnerable to corruption – Experts

While experts express concern over the general rising debt profile of Nigeria, some believe multilateral loans, which more often than are not targeted at major infrastructural projects, are susceptible to corruption.

Besides, they come with some conditionalities which make the country to be at their beck and call, they said.

Professor Garba Sheka, a Professor of Economics at Bayero University, Kano (BUK) said most of the loans from multilateral institutions have conditions attached.

He, however, stated that the government is left with no other option than to take the loan to create legacy projects.

“They have already given us conditions and we are following the conditions and we are suffering for those conditions and they are praising the government for the removal of subsidy and allowing naira to devalue.

“You must have heard the IMF praising Nigeria and they have already given them approval for additional loans. To collect the loans, you have to be abiding by their conditions. Now, they agreed that Nigeria is on the right track and they have to give us more money,” he said.

He, however, cautioned that the rising debt profile should be of serious concern to the government.

“It is recommended that countries should not collect loans that they would be servicing with more than 40 per cent of their GDP. But we are almost there. We have taken so much that the amount we are paying back is almost 40 per cent of our GDP. So there is a cause for alarm because this year alone we are going to pay back about N15 trillion, N16 trillion,” he said.

Also, another economist who pleaded for anonymity, said the rate at which multilateral organisations lend to Nigeria and other African countries is high.

He said the only relief is that the loan has long years of repayment and extended moratorium, adding, “Most of these loans would be repaid by our brothers and sons. Some of them (loans) are 25 years, 30 years.”

He stated that interventions from multilateral organisations like the World Bank in the form of loans are susceptible to mismanagement and corruption, saying the deliverables are not “measurable.”

“Most of these multilateral debts cannot be traced to any infrastructural development which we need. You can’t trace it to concrete projects with measurable impact unlike the China loan which we used to build some infrastructure.

“They (multilateral) are not concrete things you can easily put your fingers on, so they are vulnerable to corruption,” he said.

‘You need World Bank/IMF, to secure long term loans’

Another economist, Dr. Oluseye Ajuwon defended the federal government, saying the loans accumulated over a period of time.

Ajuwon of the African School of Economics (ASE), Abuja, noted that what the federal government under Tinubu has done is to restructure the loans secured by the last administration.

He recalled that at a time many companies threatened to exit Nigeria because they could not repatriate their money, saying government was able to clear some of the obligations through the foreign loans they got.

“When people say why are they borrowing money? They have to borrow money because without that, by now we would have gone under the ground with the way the economy of this country was wrecked by past administrations. We are still floating because of the good management of the economy.

“This current government is laying a solid foundation as well as reflating the economy. Imagine all the international flights saying they are not coming again, how will people be able to continue business, how will investors come into the country. So people should understand that there was a lot of financial mismanagement that was on the ground that needed to be cleaned up,” he said.

According to him, there was nothing wrong with taking loans from the World Bank or IMF, as those are the only institutions that could provide long term loans. (Daily trust)