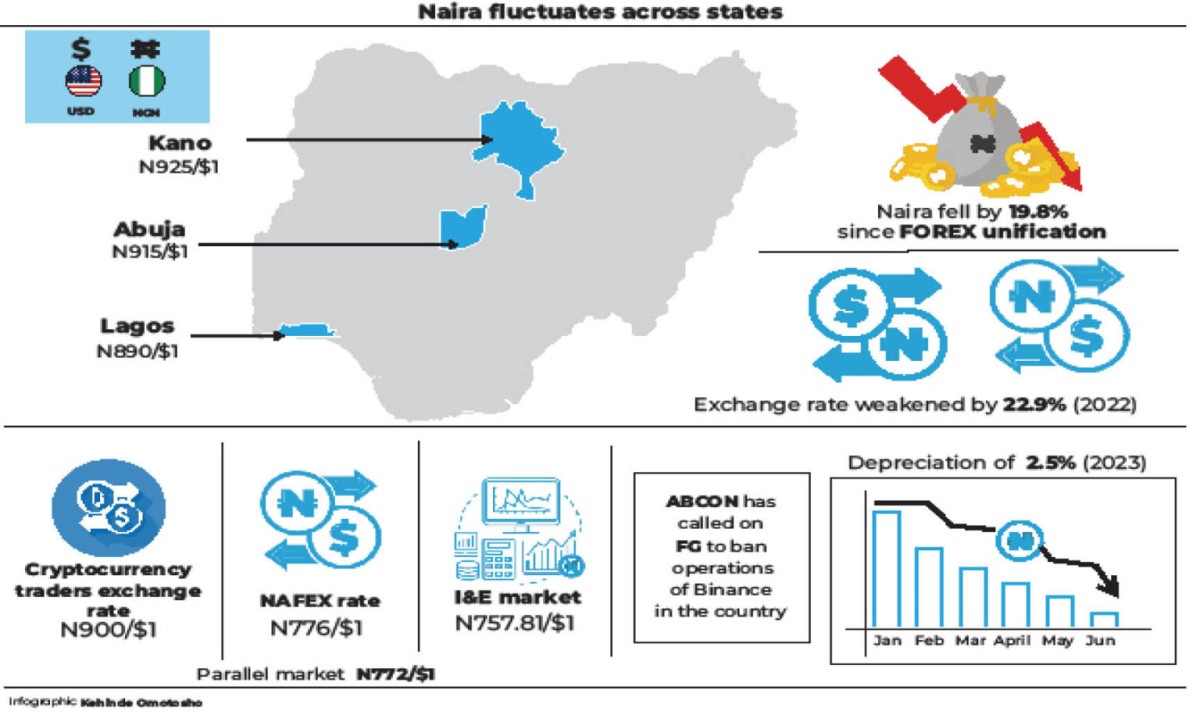

The naira plunged to a record low of N925/$1 on the parallel market on Wednesday as demand for foreign currency outstripped supply.

This is the aftermath of liberalising the foreign exchange regime, which is a clear departure of what obtained during the President Muhammadu Buhari- led administration.

At a time during the last administration, the World Bank and other agencies, as well as experts in banking, finance and economy had at different times said having official and parallel value for the naira was hurting the economy and at the same time making a few privileged people pocketing billions of dollars without producing anything as they get the forex from the CBN at official rate and instantly sell same at the black market.

Recall that during his inauguration on May 29, 2023, President Tinubu had said, “Monetary policy needs a thorough house cleaning. The Central Bank must work towards a unified exchange rate. This will direct funds away from arbitrage into meaningful investment in the plant, equipment and jobs that power the real economy.”

On June 14, 2023, the CBN abolished the segmentation of the forex market into different windows and told Deposit Money Banks to freely float the naira against the dollar and other international currencies.

Buyers and sellers of foreign currency in the official FX market were then allowed to quote their preferred rates, as against previous practice where CBN dictated rates.

Wittingly or unwittingly, naira has since continued on a free fall at the parallel market despite the move.

When Daily Trust reached out to forex traders in Abuja yesterday, they quoted the exchange rate as high as N915/$1 for cash trades.

Similarly, the dollar exchanged for between N880 and N890 in Lagos, the commercial capital of Nigeria.

Our reporter who monitored the situation at the Murtala Muhammed International Airport, Ikeja as well as Allen Junction, noticed that the greenback was bought for as high as N890 by Bureau De Change operators in the state. However, the operators sold it for between N900 and N905.

An operator at Allen Roundabout in Lagos, Ismail Muhammed said: “The dollar has not reached N900 in Lagos. We are buying for N890 at the moment”.

In Kano, Daily Trust gathered that while the parallel market closed on Tuesday with a dollar trading to a naira at N900, it opened at N919 to a dollar on Wednesday as against the N750.2/dollar at the I&E market, signifying a gap of about N169 between the parallel market and the I&E market.

However, Daily Trust gathered that around 1pm, the price further surged in Kano’s Wapa Forex Market to N925 to a dollar.

I & E window closes at N757/$1

Meanwhile, in the official Investor and Exporter Window, the exchange rate closed at N757.81/$1 while the NAFEX rate was N776. The official market also faces supply constraints, with daily turnover averaging $80 million since July.

The peer-to-peer market, where cryptocurrency traders exchange forex, also saw the exchange rate soar above N900/$1.

Naira falls 19.8% since Fx unification

The exchange rate between the naira and dollar has weakened by 19.8% since the reunification of the exchange rate windows. This compares to a depreciation of 2.5% between January 1 and June 14th (before the unification). The exchange rate weakened by 22.9% in the whole of 2022.

The disparity is now N153/$1, one of the widest since the unification of the naira on June 14th, 2023.

The naira has been under pressure in the parallel market for several weeks, as the supply of forex from official sources remains inadequate.

On July 1st, the beginning of the second half of the year, the exchange rate in the parallel market was around N772/$1.

However, a surge in demand from various segments of the economy, such as importers, foreign travellers and speculators, has triggered exchange rate volatility.

‘Scarcity major factor’

Daily Trust spoke to some forex traders who attributed the depreciation of the naira to a scarcity of supply.

They said that there were more buyers than sellers in the market and that the situation was unlikely to improve anytime soon.

A forex dealer, Nura Usman told Daily Trust that it was scarcity and lack of price control mechanism that was responsible for the astronomical rise in the exchange rate and the huge gap between the official and parallel markets.

“Even commercial banks do not have dollars, they come to us to look for it when their customers ask for it. So, this makes you wonder why CBN is not contributing its quota to the market. If the CBN releases dollars to the commercial banks at the I&E price, definitely the gap between the I&E market and our own (parallel) won’t be more than N10 and not the over N160 that we currently have,” he said.

Usman added that the chances are very high that a dollar will go above N1, 000 sooner than anticipated if nothing was done to quickly address the scarcity.

Also speaking, the Chairman of WAPA Forex Market, Sani Dada said the government is to be blamed for the scarcity and huge gap between the I&E market and the parallel market.

He said Nigeria is not productive enough to be getting the required forex the market needs and as such the floatation of price without commensurate supply of dollars to the market by the government was counter-productive.

“For us, our only source of dollars now is from travellers who will bring some hundreds of dollars to you. Even yesterday (Tuesday), I needed $1,000 and I couldn’t get it anywhere in the market. That is how bad things have gotten. So, the government needs to release some percentage of dollars to operators (BDC) as it was done in the past so that it can reach the people that truly need it,” he said.

Oyinlola Oluwafemi, a commercial bank customer said: “We really need to diversify our foreign exchange earnings from just oil so that we can have much more surplus supply of dollar, as for the demand for foreign exchange, it is not going to go away anytime soon so we have to deal with that.

“Another factor affecting the gap is the official bottlenecks that exist in our banking system. Imagine applying for PTA for 14 days prior to need, that is too long a time to wait.”

BDCs urge FG to ban Binance operations

However, the Association of Bureaux De Change Operators of Nigeria (ABCON) has called on the federal government to ban the operations of Binance in the country.

Binance is a global online exchange where users can trade cryptocurrencies on a daily basis. It supports hundreds of the most commonly traded cryptocurrencies.

President of ABCON, Alhaji Aminu Gwadebe in a chat with Daily Trust, said Binance trading is becoming the anchorage of the Investor and Exporters window and the parallel market, noting that the exchange is the most liquid market with 1.2 million transactions per second.

He said: “So, we have to do something that can stop Binance. It’s a competition; we need to ban Binance and the only way to do so is if you have liquidity.

“So we are seeing a scenario where optimism is giving way to pessimism; investors are not coming, Nigerians don’t have confidence in the market and we have to look for external finances that are coming in as a quick fix.

“There is a lot of pressure on the naira, from foreign exchange hoarding by the banks and oil companies.”

CBN expects remittances from NNPC

Gwadabe expressed hope that with the petrol subsidy removal, the Central Bank of Nigeria would be able to see remittances from the Nigerian National Petroleum Company Limited (NNPCL) saying at the height of subsidy on oil, the remittance to CBN from NNPC was zero.

He said now that the situation has changed, this would also allow the apex bank to have liquidity and inflows that would come in for them to be able to defend the naira.

He said: “If we have a friendly, competitive and transparent system, more investors would want to come to the market.”

Official window no longer reflective of the market dynamics

Ayodele Akinwunmi of the Corporate Banking Department of First Securities Discount House Limited (FSDH), said: “The way things are today, we have to be careful with what we quote as the spread in the parallel market. The fact that the CBN says we can buy and sell at any rate does not give room for arbitrary price quotes.

“As much as I know, the CBN has been selling dollars to the Import and Export window consistently at N740/$1. The supply may not be enough considering the huge backlog; the reference rate is still the I&E window.

“It is a matter of demand and supply and with what the government is doing, the rates will decelerate in no distant time”.

However, the Managing Director of Cowry Asset Management, Dr Johnson Chukwu said the basic underlying factor in the continuous widening of the gap between the I&E window and the parallel market is undersupply.

Chukwu, while reacting to the stability in the I&E window amidst wide drift in the parallel market, said: ‘The official market is no longer reflective of the market dynamics.

“In effect, the I&E window is no longer indicative of demand and supply, the price is stable because the offer and bid price are determined by the CBN.”

Reacting to what the government can do to arrest the free fall, Chukwu said: “We are already in a bind, I don’t see the federal government accepting a short-term balance sheet support.

“We are heading towards a point where dollarisation will kick in. I don’t know where that point is right now but we are in a deep mess.”

We need to work on the supply side of fx-CBN

The CBN Director of Corporate Communications, Dr Abdulmumin Isa, in his reaction, said: “While we will continue to intervene to bring the markets to the levels that we believe it should be, we need to work on the supply side of forex to the economy.

“As the Ag CBN governor, Folashodun Shonubi, said at the last MPC meeting, some of the volatility you’ve seen over the period has been driven by that same fact that the market needs to find its level and also the reality that there’s pent-up demand, which current supply may not be sufficient for and as we ease and satisfy the pent-up demand, we begin to see a more efficient market that runs.” (Daily Trust)