Business

Digital loans, digital trauma: Inside Nigeria’s lending boom and its toll on mental health

A petty trader in Ojota, Lagos, Oghenekaro Onome’s life took a terrifying turn one ordinary day. Her daughter, a curious teenager, picked up her mother’s phone and applied for a N50,000 loan from a popular digital lending app without permission.

The money hit the account almost instantly. When Onome discovered the transaction, she was furious but relieved, she did not need the money and wanted to return it immediately. The app refused a full refund. They insisted she must pay interest for that single day.

Desperate, she involved her sister, a journalist. Only then did the founder of the app intervene and provide his personal account details for the return. Onome transferred the money back promptly.

What followed was a nightmare. The company claimed she had sent the funds to the wrong account. Aggressive calls flooded her phone with threats. They warned that if she did not repay, they would print her name all over the internet and accuse her of murder. The harassment continued relentlessly until she changed her phone line to escape the fear. Even today, the memory brings anxiety and distrust of technology.

This is not an isolated incident. Across Nigeria, digital lending apps have created cycles of easy credit that quickly turn into debt traps, public shame, harassment, and deep mental stress.

In October 2023, the nation was shocked by the suicide of Sanni Hameedat (also reported as Hameedah), a 20-year-old 300-level Microbiology student at the University of Ilorin. She reportedly took her life after struggling with a N500,000 debt linked to online lending pressures.

While details sometimes vary in reports (some linked it to lending money to an online acquaintance), the case highlighted how debt from digital sources can push vulnerable young people to despair. Her death became a symbol of the hidden human cost of easy loans.

Such tragic cases, though not always officially tallied as loan-app specific, illustrate the extreme risks.

Consider Chinedu (surname withheld), a young professional in Abuja. He borrowed N30,000 to pay his monthly house rent. A missed deadline triggered messages to his entire contact list, including colleagues, family, and friends, labeling him a thief.

The shame cost him respect at work and strained family ties. He borrowed from a second app to repay the first, then a third.

Sleepless nights, constant fear of calls, and social withdrawal followed. “I feel like a prisoner in my own life,” he shared anonymously.

These human stories reveal a deeper crisis in Nigeria’s digital lending sector.

The rise of digital lending apps

According to market data from industry research firm, The Business Research Company, the global instant loan application market was valued at approximately $4.48 billion in 2025, reflecting the rapid growth of digital lending services worldwide. The expansion has been driven by increasing smartphone penetration, improved digital payment infrastructure, and rising demand for quick, unsecured credit, particularly in emerging markets.

In Nigeria, one of Africa’s most active digital lending markets, the consumer digital lending sector is estimated to be worth about $2.1 billion, with 425 registered loan apps operating in the country as of mid-2025, according to industry and regulatory data.

Meanwhile, data from mobile app intelligence platform, Sensor Tower, shows that revenue generated by the world’s top 500 finance apps, including mobile banking, payment, and digital credit platforms, grew by 10.2 percent to approximately $407.3 million, underscoring the increasing global adoption of digital financial services.

Nigeria’s digital lending exploded because of its speed and accessibility. Apps promise fast loans with no collateral, minimal paperwork, and instant approval via mobile phones. They target salary earners, university students, and informal sector workers who often cannot access traditional bank credit.

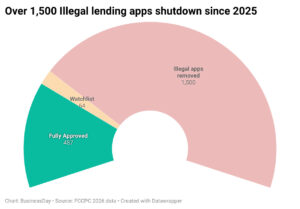

By early 2026, hundreds of players operated in the market. Following the January 5, 2026 compliance deadline under the the Digital, Electronic, Online and Non-Traditional Consumer Lending Regulations (DEON 2025) Regulations, 521 digital lender companies came under the Federal Competition & Consumer Protection Commission (FCCPC) oversight, with 457 holding full approval.

Dozens more operated conditionally or faced watchlist status. Over 1,500 illegal lending websites and apps have been shut down in enforcement drives from late 2025 into 2026.

Loans are often short-term, days or weeks, with high effective interest rates that can reach 20 percent to 30 percent monthly or far higher when compounded with fees.

The debt spiral

The pattern is predictable and painful. A borrower misses one deadline and borrows from App B to pay App A. Late fees and compounding interest turn small amounts into unmanageable burdens. A N10,000 loan can balloon rapidly. Many juggle three or more platforms at once.

This spiral worsens amid Nigeria’s cost-of-living crisis. High inflation, rising food and transport costs, expensive rent in cities like Lagos and Abuja, school fees, and medical emergencies leave families with few options.

Informal workers and young professionals living paycheck to paycheck turn to apps for survival.

The harassment economy

When repayment fails, some apps unleash aggressive recovery. Repeated calls, threatening messages, and most damaging, contact shaming.

Recovery teams send messages to family, friends, and workplace contacts accusing borrowers of fraud or warning others against them. Some send fabricated criminal photos or defamatory claims.

“These tactics create psychological pressure that often forces payment. They also destroy relationships, reputations, and careers,” mental health experts averred.

Mental health impact: A silent crisis

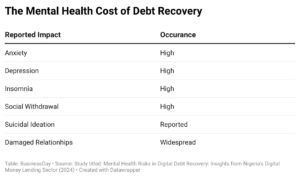

The psychological toll is severe. A key 2024 study titled “Mental Health Risks in Digital Debt Recovery: Insights from Nigeria’s Digital Money Lending Sector” provides one of the clearest academic examinations of how aggressive debt recovery practices by digital lenders affect borrowers’ mental health.

Using a qualitative scoping review of victim accounts, the research systematically analysed cases of cyber coercion in the digital lending space.

“The results showed that digital money lenders in Nigeria use various stigmatizing tactics, including debt-shaming, cyberbullying, and defamation of character, to recover funds from debtors. These tactics have negative implications for the mental health of debtors, including depression, anxiety, and suicidal ideation,” Oyeleke Johnson, the author of the study stated.

The study found that these practices go beyond simple reminders and often involve public humiliation through contact lists, fabricated accusations, and relentless digital harassment. Many victims described living in constant fear, social withdrawal, insomnia, and eroded self-worth.

The research highlighted how easy access to credit quickly turns into psychological warfare when repayment fails. Borrowers, particularly salary earners, students, and informal workers, face compounded stress from multi-app borrowing cycles and aggressive recovery methods.

Oyeleke noted that while short-term loans provide temporary relief amid economic hardship, the recovery tactics create long-term trauma that affects relationships, work performance, and overall well-being.

“The findings revealed a pattern where shame-based recovery not only pressures payment but leaves lasting emotional scars. Secondary victims like family members and colleagues targeted with shaming messages, also suffer damaged trust and emotional distress,” Oyeleke explained in the paper.

The author emphasised that these tactics constitute a form of cyberbullying with measurable mental health consequences.

The Nigeria Data Protection Commission (NDPC) reported investigating over 400 cases of severe privacy breaches and cyberbullying linked to digital lenders as far back as 2024.

High-profile suicides, like the UNILORIN case, and widespread anecdotal reports from victims and advocates point to a broader crisis.

Why people still borrow

Driven by a severe cost-of-living crisis, the financial habits of Nigerians have shifted dramatically. Economic pressures have forced a massive portion of the population to use loan apps not for luxury, but for basic survival.

The macroeconomic landscape directly drives the necessity for instant digital credit, as household incomes fail to keep pace with basic costs.

Headline inflation: Data from the National Bureau of Statistics (NBS) indicates that headline inflation sits at 15.69 percent, with food inflation remaining a primary driver at 16.06 percent. This persistent pressure heavily erodes daily purchasing power.

Poverty rate: The World Bank and financial advisory reports from PwC Nigeria reveal that poverty levels have climbed from 62 percent to 63 percent. This means approximately 141 million Nigerians live below the poverty line, stripped of financial safety nets.

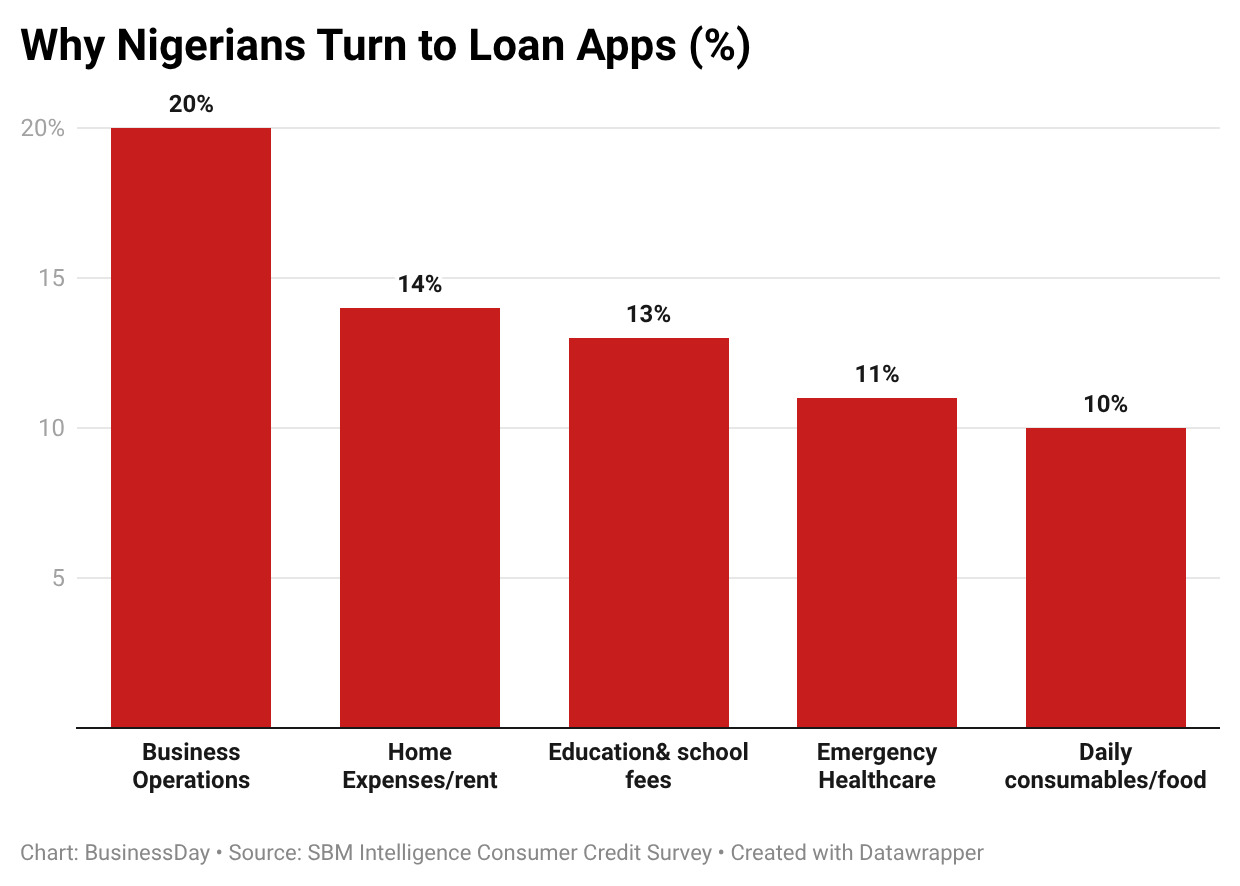

The living expense trap: Research by SBM Intelligence reveals that 27 percent of Nigerians across various income brackets regularly resort to digital loan apps strictly to maintain standard living expenses and purchase food.

Business expenses: Micro-entrepreneurs and market traders require rapid capital injections to replenish inventory due to volatile, fluctuating wholesale prices.

Home improvements & rent: Landlords in urban hubs typically demand upfront, annual rent payments, forcing tenants to seek quick credit.

Education & tuition: Families use quick loans to cover sudden school fee deadlines, text books, and exam registrations to prevent children from being sent home.

Healthcare & emergencies: Unexpected medical bills require instant cash, especially given low health insurance penetration across the country.

High cost of traditional credit: Regulated commercial banks feature benchmark interest rates around 27.5 percent, which can drive conventional personal loan rates as high as 48 percent annually. Loan apps exploit this by promising deceptively fast processing, despite hiding astronomical rollover fees.

According to CBN data, outstanding personal retail loans across the country surged over 21 percent in a single quarter, standing at a massive N3.82 trillion. This highlights a broad, systemic reliance on credit to cushion severe economic shocks.

The DEON Response

For years, weak oversight allowed abuses. Many apps operated across borders or without strong local accountability. Borrower protections were limited.

In July 2025, the FCCPC introduced the DEON 2025. The rules demand registration, transparent terms, fair interest disclosure, data privacy, and ethical recovery practices.

While there is no fixed interest ceiling, the FCCPC enforces its general consumer rights and fair lending rules with heavy statutory punishments. Lenders who practice deceptive pricing, hidden rollovers, or abusive recovery face fines up to N100 million or one percent of their annual turnover; a 5-year disqualification for company directors and immediate removal from the approved digital lenders list and app stores

Tunji Bello, FCCPC executive vice chairman explained that the regulations address longstanding consumer complaints about exploitative practices, privacy violations, and abusive recovery tactics.

By January 2026, enforcement removed non-compliant operators from approved lists, with phased actions against over 100 unregistered apps. While court challenges occasionally slow progress, the Commission continues pushing for compliance. Early signs show some reduction in overt abuses, but many borrowers still report lingering issues.

Bayowa Fredrick Borokini, founder and chairman of Andray Finance, emphasizes ethical lending, stating, “For too long, the digital lending space in Nigeria has been clouded by predatory practices… We are offering a sanctuary for borrowers — fast, fair, and respectful of individual dignity.”

Borokini, in an interview with BusinessDay, said his platform avoids contact harvesting and uses data analytics responsibly to build credit histories for underserved groups like mechanics and traders.

James Edeh, head of compliance at FairMoney Microfinance Bank, notes that compliance is the new currency, adding that institutions adhering to DEON, NDPA, and CBN rules build trust.

FairMoney reported strong growth and credit rating upgrades in 2025, funding much of its book through deposits from confident customers, Edeh revealed.

The bigger picture

No doubt, digital lending apps form part of Nigeria’s survival economy. They fill gaps left by weak social safety nets and limited formal credit.

Yet they also reshape relationships. Trust erodes when shaming messages reach family and colleagues. Work life suffers. Mental health bears a silent, heavy burden.

Technology that lowers barriers to credit must include strong guardrails. Without them, easy loans become fast traps.

The DEON regulations represent progress, but enforcement, public education, and ethical innovation will determine real

Oyeleke the researcher called for urgent regulatory and societal action. “My study recommends that the Nigerian government should enforce existing laws and regulations to protect debtors from unethical practices of digital money lenders.”

He advocated for stronger enforcement of consumer protection rules, public awareness campaigns on borrowing risks, better mental health support services for affected individuals, and ethical guidelines for fintech recovery practices that respect human dignity.

The researcher stresses that without decisive intervention, the mental health crisis linked to digital debt recovery will continue to deepen.

Other stakeholders advised that stronger, consistent enforcement is essential, adding that consumer education on risks, transparent terms, and borrowing limits can help, while advising fintechs to adopt dignity-respecting recovery methods.

FCCPC boss advised Nigerians that, “If you or someone you know faces harassment, report to the FCCPC via their website. File privacy complaints with the Nigeria Data Protection Commission. Seek mental health support from organizations like the Mentally Aware Nigeria Initiative (MANI).”

Nigeria’s digital finance revolution holds great promise. But it must prioritize people over profits. As enforcement of DEON rules continues through 2026 and beyond, the true measure of success will be fewer stories like Mrs. Onome’s, fewer debt spirals, and healthier lives for ordinary Nigerians. (BusinessDay)

-

News11 hours ago

News11 hours agoPFIPC: CBN opens govt accounts only on OAGF authorisation – Director tells Reps probe panel

-

News11 hours ago

News11 hours agoHow PFIPC got into 2026 Budget — Adeyemi

-

Metro11 hours ago

Pastor to die by hanging for killing 16-yr-old daughter in Calabar

-

Politics11 hours ago

2027: Kwankwaso confirms written one-term agreement with Obi

-

Sports23 hours ago

Ex-England captain, manager Kevin Keegan dies following battle with cancer

-

Sports21 hours ago

“The pain is immense,” says Messi of World Cup defeat

-

Business8 hours ago

Consensus On CBN Holding Rates At 26.5% Ahead MPC Decision

-

News22 hours ago

Tinubu appoints Fayose Chairman Rural Electrification Agency, make 25 other appointments