Opinion

How Economic Policies Built Africa’s Richest Man — And Why Nigeria Needs That Policy Mind Again

By Kunle Oshobi

There was a time when Nigeria dreamed in confident colours.

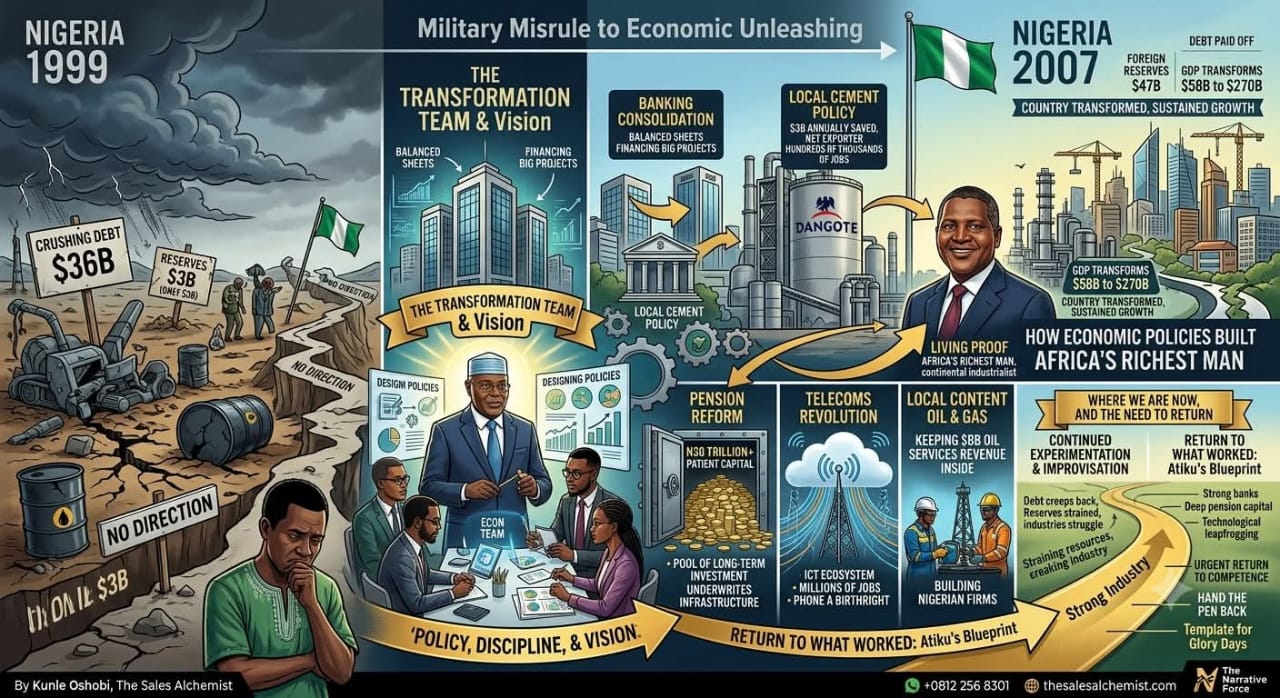

Picture the country in 1999. The military had just handed over power after decades of misrule. The treasury was a shell. Nigeria owed the world $36 billion it could not pay. Foreign reserves, the nation’s rainy-day fund, stood at a humiliating $3 billion. Inflation was biting. Unemployment was rising. Investors looked at Nigeria the way a banker looks at a customer with a maxed-out overdraft: politely, but with the door already closing. Then something changed. Not by accident, but by design.

The Team That Rebuilt a Nation

At the heart of that turnaround was a National Economic Council chaired by a Vice President who understood that government’s job was not to control the economy, but to unleash it. Atiku Abubakar was handed one of the most consequential assignments in Nigeria’s history: assemble the economic team that would decide whether this country sank or swam. He gathered some of the sharpest minds the nation could find and set them loose on the problems everyone else had been too timid, or too compromised, to touch.

What followed was not luck. It was policy, discipline, and vision, stacked year upon year.

The banks got stronger. Through banking consolidation, dozens of fragile, undercapitalized banks were forced to merge into fewer, far stronger institutions, banks with the balance sheets to finance the kind of big-ticket, multi-billion-dollar transactions that build refineries, power plants, and factories, not just fund market women’s working capital.

Cement stopped bleeding the treasury dry. A deliberate local cement policy backed local manufacturing instead of endless importation. The result: roughly $3 billion a year that used to leave the country to pay foreign cement producers began staying home. Nigeria didn’t just stop importing cement, it became a net exporter, and hundreds of thousands of jobs sprang up around factories, logistics, distribution, and construction.

Retirement stopped being a death sentence. Pension reform created, from almost nothing, an industry that has since grown into a pool of long-term investment capital exceeding thirty trillion naira, the single largest reservoir of patient capital in Nigeria’s entire financial system, money that today underwrites infrastructure, housing, and industry.

A phone became a birthright, not a luxury. The telecoms revolution turned a country where owning a landline was a mark of privilege into one of the fastest-growing mobile markets on earth, birthing an entire ICT ecosystem and creating millions of jobs that didn’t exist a decade before.

Nigerian oil workers stopped being spectators in their own industry. Local content policy in the oil and gas sector fought to keep a significant share of the roughly $8 billion once paid annually to foreign oil service companies inside the country, building the capacity of Nigerian firms instead of permanently subcontracting the nation’s most valuable resource to outsiders.

And the debt, the crushing, generational debt, was paid off. Nigeria’s credit standing improved. Investors who had written the country off started paying attention again. Foreign reserves, that $3 billion embarrassment of 1999, climbed to roughly $47 billion by 2007, the single greatest accumulation of national savings in Nigeria’s history, built in eight years.

The Numbers Tell a Story Numbers Rarely Tell

By the time that administration left office, Nigeria’s GDP had grown from a paltry $58 billion in 1999 to $270 billion in 2007. That is not a modest improvement. That is a country transformed, the longest, strongest sustained period of economic growth Nigeria has ever recorded, before or since.

But numbers on a page don’t capture what this meant on the ground. It meant a young graduate could get a bank job at an institution that could compete regionally. It meant a trader could get a mobile line and start doing business by phone instead of trekking across town to confirm an order. It meant a retiree could believe, for the first time, that there might be something waiting for them after decades of service. It meant a nation that had been begging for debt relief could instead start looking outward, at what it could build next.

The Man Who Became Africa’s Richest, Because Nigeria Got Its Economics Right

Here is a story too many Nigerians have never connected the dots on: Aliko Dangote, Africa’s wealthiest man, has himself pointed to that era’s cement policy as the seed of his empire. It was that policy that gave him the room to build the local cement capacity that made him a continental industrialist. It was those same newly-consolidated, muscular Nigerian banks, strengthened directly by the reforms of that administration, that had the balance sheets to finance his expansion when nobody else could write him the kind of cheques he needed.

Without that foundation, there is no mega cement empire. Without that foundation, there is no financing base sturdy enough to bankroll the Dangote Refinery, a project so large it has reshaped conversations about African industrial capacity. Dangote’s fortune is not just a story of one man’s ambition. It is living proof that when Nigeria gets its economic policy right, it doesn’t just lift the country, it can produce the richest man on the entire continent while creating millions of jobs in the process.

Where We Are Now, and What We Are Missing

Ask any Nigerian today, young or old, whether the country feels like it is moving in that same direction, and you will struggle to find one who says yes with confidence. Reserves that once climbed are strained. Debt that was once paid off has crept back, and then some industries that were carefully nurtured now struggle for survival. A generation of young Nigerians is asking, with real urgency, whether this country still knows how to grow.

The tragedy is not that Nigeria lacks the blueprint. The tragedy is that the blueprint has been sitting there, tested and proven, while the country keeps improvising instead of returning to what worked.

Why Atiku, and Why Now

This is not a story about nostalgia. It is a story about competence that has already been demonstrated, under real pressure, with real results, on the largest and most difficult stage in the country, the Nigerian economy itself.

Atiku Abubakar did not simply witness that era of growth from the sidelines. He was handed the responsibility of assembling and directing the team that engineered it. He has already done, at national scale, the single hardest thing any Nigerian leader can be asked to do: take a broke, indebted, directionless economy and turn it into one of the fastest-growing in the world, in less than a decade.

Nigeria does not need another leader who is still learning on the job while the country’s fortunes hang in the balance. It needs someone who has already proven, with a track record the whole world can check, that he knows how to build the team, design the policy, and deliver the growth.

The glory days were not an accident of high oil prices or good fortune. They were built, deliberately, by people who understood how economies actually grow, through strong banks, local industry, deep pension capital, technological leapfrogging, energy sector empowerment, and fiscal discipline that earns a nation’s word back on the world stage.

Nigeria has seen what is possible. The question now is simple: does the country want to keep experimenting, or does it want to return to the hands that already proved they know how to build?

The glory days are not history. They are a template, and Nigeria needs, urgently, to hand the pen back to the man who helped write them the first time.

Kunle Oshobi is the Head of Strategy and Planning, and Chairman Narrative Command of The Narrative Force.

-

News22 hours ago

News22 hours agoGbajabiamila-Adeyemi Saga: Why National Assembly appropriated ₦1.3bn for fake agency – Senate spokesperson

-

News20 hours ago

Kwara: Abducted Worshippers Regain Freedom After 105 Days In Captivit

-

News21 hours ago

Nigeria’s recovery faces its biggest test yet

-

News20 hours ago

I deposited billions in cash for Emefiele – Witness tells court

-

World News19 hours ago

UK lawmaker Nigel Farage resigns over £5 million gift controversy

-

News12 hours ago

EFCC hands over 1,452 recovered items to Unity Schools

-

News19 hours ago

Court adjourns trial of six alleged coup suspects until July 20

-

News20 hours ago

My Husband Doesn’t Deserve This Persecution – El-Rufai’s Wife Tells Tinubu