Business

Lenders Balk At Amukpe-Escravos Pipeline Sale At Old Valuation

Lenders, including Sterling Bank, Keystone, and others, are objecting to reviving a previously scrapped plan to acquire a stake in the Amukpe-Escravos Pipeline, questioning the rationale behind moving up a September 2025 approval tied to the failed deal.

The prior approval indicated a lower bid, and lenders are reportedly advocating for an independent advisor to manage the asset sale, which is currently valued at approximately $600 million.

The sale between Continental Oil and Gas Limited and Conpurex Limited was terminated in October 2024 due to missed payments, unresolved breaches, and attempted alterations to the agreed-upon terms that would have shifted core risks to the seller.

By the time it ended, the process had stalled and lost credibility with financial stakeholders.

However, the reappearance of a prior approval tied to that process is worrying lenders, who fear a closed deal is being reopened without the customary procedural reset.

A lender told InsideBusinessNG that the correct way to revive a failed transaction is to start over with a new valuation before reopening the 40 per cent stake to new bids.

Without a new valuation, the industry now considers the development a significant commercial issue, with stakeholders saying it has moved beyond a typical transaction dispute into something that tests how Nigeria handles valuation, process integrity, and national interest when strategic assets are involved.

For lenders and other stakeholders, it has become a test of governance and institutional discipline, particularly given the asset’s strategic importance.

In recent years, the Amukpe-Escravos Pipeline has become a vital evacuation route, especially as challenges with other corridors have continued. With a capacity of 160,000 barrels per day and uptime consistently above 95 per cent, it’s seen as a valuable piece of infrastructure, with pricing expected to reflect both its strong performance and strategic importance.

The valuation is now at the heart of the dispute, with reports suggesting the original $243 million offer had already faced pushback from a group of lenders who doubted the assumptions behind it.

Their concern was that the valuation did not align with the asset’s operational reality or prevailing market conditions.

An independent assessment conducted in 2025 places the same stake significantly higher, with estimates approaching $600 million under reasonable assumptions.

The difference is substantial and, in the context of a strategic national asset, raises clear concerns about value preservation.

For lenders, the implication is direct. Proceeding based on the earlier benchmark risks locking in a transaction at a level materially below the current market value.

The challenges go beyond just pricing. According to industry sources, the earlier transaction took place during a time when key financial stakeholders weren’t fully on the same page.

Subsequent restructuring of the financing framework, supported by improved coordination between lenders and relevant institutions, has since introduced clearer parameters for how any divestment should be undertaken

Following the exit of the original bidder, Conpurex Limited emerged without a clearly defined transition process, then failed to meet its financial commitments while seeking to reopen settled terms.

Among the proposed revisions were provisions to transfer regulatory approval risks back to the seller and to introduce interest claims on refundable sums.

Lenders describe these as commercially untenable and indicative of a process that had become inconsistent.

What now concerns the syndicate is not simply that the deal failed, but that a process widely regarded as compromised is being given a renewed effect through administrative carryover.

In private discussions, the concern is framed more starkly. If a terminated transaction can be revived without a formal restart, the distinction between concluded and ongoing processes begins to erode. That, in turn, weakens contractual certainty and introduces caution into capital allocation decisions.

For institutions already exposed to the asset, the risk is immediate.

Lenders are understood to be pressing for a reset. Their position is that the September 2025 approval should be revisited rather than implemented. A process that has lost both commercial coherence and procedural integrity, they argue, cannot form the basis of a binding outcome.

The proposed path forward is straightforward. Reverse the approval, appoint an independent adviser, and return the asset to the market through a transparent and competitive process that reflects current value.

They caution that anything less risks a precedent where processes can be retroactively adjusted, valuations can deviate from reality without consequence, and disciplined asset transfer becomes subjective.

For an industry built on long-term capital and measured risk, that is not a trivial signal. It is a defining one.

-

Politics3 hours ago

Politics3 hours agoOgun APC unveils Yayi’s running mate

-

News3 hours ago

Power debt: Tinubu’s N4trn bond is a racket, says Atiku

-

News24 hours ago

Activist Nwapa Lambasts Katsina Governor For Pampering Bandits After Major General Rabe Died In Terrorists’ Den

-

Business24 hours ago

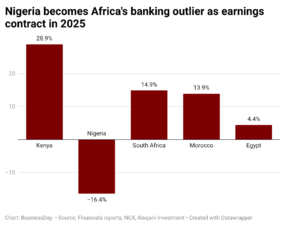

Business24 hours agoNigeria becomes Africa’s banking outlier as earnings contract in 2025

-

World News3 hours ago

US, Iran reach peace deal, signing set for Friday

-

Opinion19 hours ago

Depression to Destiny: The Abdulsalami story

-

News24 hours ago

Kogi Government Bans Okada, Imposes 7pm Curfew In Parts Of Kabba, Bunu Council Over Bandit Attacks

-

News16 hours ago

Fulani settlers abandon southern communities, cite ethnic profiling